Retirement Account Basics: Why You’re Never Too Young to Start Thinking About Retirement

"Retirement is wonderful if you have two essentials—much to live on and much to live for."

—Anonymous

Why Should You Think About Retirement Now?

Did you know that the average American spends 20 years in retirement?1 How much money do you think you would need to save to live off of for 20 years if you weren't working? It can feel like retirement is so far away that you don't need to save. And even a quick internet search on retirement planning can generate an overwhelming number of options and advice.

In this essay, we will explore some of the most common retirement savings plans and things to consider when thinking about retirement. By understanding some of the basic forms of retirement savings accounts, you'll be more prepared to start making decisions for the future.

What Are My Retirement Savings Options Through an Employer?

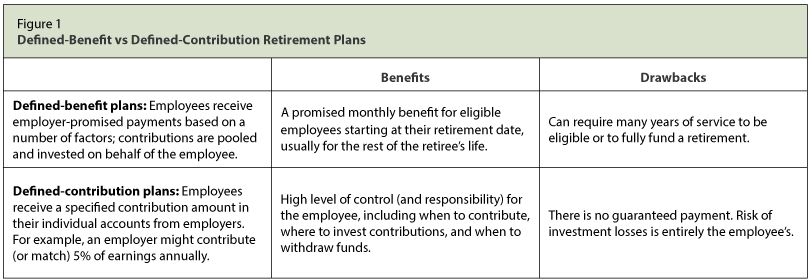

Employer-based retirement savings plans generally fall into two categories—defined-benefit and defined-contribution plans (Figure 1).

In a defined-benefit plan, commonly called a pension plan, the employer sets aside money for eligible employees and invests those funds on their behalf. Employees are promised a monthly payment when they retire based on several factors, including salary and length of service. Employees don't have any responsibility (or opportunity) to choose how the money is invested. The promised payments for the employee's lifetime make them an attractive job benefit, but they often require long terms of service with the employer.2

In a defined-contribution plan, the employee, not the employer, sets aside money and decides how to invest those funds. The most common defined-contribution plan is a 401(k). The employee puts money from each paycheck into their retirement savings account and selects investment choices (usually from an approved list of mutual funds). These plans offer a higher level of choice for the employee, including when they may withdraw money during retirement. To create an incentive for employees to save, many employers will match the amount employees contribute up to a certain percentage.3

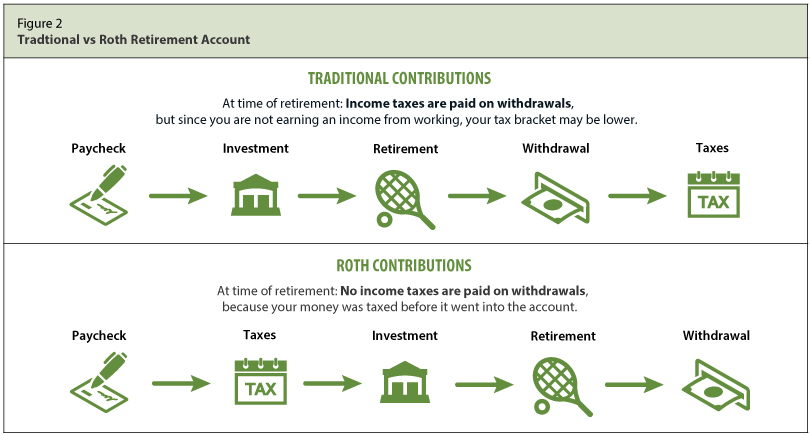

Defined-contribution plans can also be categorized based on how they handle taxing the contributions. In each case, the saver is taxed; the difference is whether investments are made with pre-tax or after-tax income.

In a traditional account, contributions are made before income taxes are paid: The investment accumulates and compounds, and the employee pays income taxes when they withdraw the money. This lowers the employee's taxable income today and potentially puts them in a lower tax rate bracket when they withdraw the funds during retirement.

In a Roth account, contributions are made after income taxes are paid: The investment accumulates and compounds, and the employee can then withdraw the money income tax-free during retirement. The advantage of this type of account is that interest earned in the account over time is essentially income tax-free (Figure 2).

Tax-advantaged accounts, such as a 401(k) plan or a Roth account, reduce your overall income tax burden and provide an incentive to put away money for retirement. But it's important to realize that the money deposited in these types of retirement accounts ideally stays there until you're 59½ years old; otherwise, you'll pay a penalty for early withdrawal, in addition to the usual income taxes on such withdrawals.

What If My Employer Doesn't Have Retirement Savings Options or I'm Self-Employed?

For individuals who do not have retirement savings options through an employer, there are still several options available. Individual retirement accounts (IRAs; Figure 3) can be opened and managed on your own through numerous financial institutions. With an IRA, you decide where to invest your funds and how much money to contribute and when. Like in defined-contribution plans, there are both traditional and Roth versions of IRAs available.

For small businesses and people who are self-employed, there are accounts beyond IRAs that have higher annual contribution limits, such as simplified employee pensions (SEPs). If you qualify for an SEP account, investing a higher amount each year can be a way to increase the total amount you save for retirement.

But What About Social Security?

According to the Social Security Administration, Social Security, on average, replaces only 40% of annual pre-retirement earnings. In other words, if Social Security were the only retirement savings you had, you would be living in retirement on a budget of approximately 40% of your working income. Most financial advisors suggest you would need 70-80% of your pre-retirement income annually in retirement.4

These averages suggest that while Social Security can be an integral part of your retirement planning, it ideally wouldn't be the only way you save for retirement.

What Type of Retirement Account/Plan Do You Want?

The number of options when saving for retirement can feel so overwhelming that you don't even want to think about retirement planning. You may want to talk with a financial advisor to help learn about and evaluate options that would be best for you. Some employers may even offer this service as part of their benefits to employees. When looking for a financial advisor, the following are a few things to consider:

- Consider your own financial planning needs and compare them with the services offered. Think about your financial goals and circumstances to determine if the services and experience of the financial advisor you are considering would be beneficial to you.

- Make sure to choose a financial advisor with a license or reputable background in financial planning. Don't be afraid to ask questions about their credentials and research the companies/firms offering you advice.

- How will the financial advisor be compensated? Most financial planning professionals earn money through fees or through commission. Fee-based services allow you to know upfront the cost of the service they are offering. They may charge based on the total value of your account (say, a fee of 1% of the account's total value), or they may charge an hourly rate or annual fee. Commission-based services allow the financial advisor to earn a commission when you buy certain products or services. This can impact the type of advice they offer, as they may be biased toward certain products. Make sure you understand how the financial advisor is being compensated, as this may impact the advice they offer you.

How To Make the Most Out of Retirement Savings

Start early! Small amounts saved over longer periods of time do add up (Figure 4). It may feel like saving a small amount of each paycheck won't make a difference, but the sooner you begin saving for retirement, the longer your investments have to earn a return. You'll also be building habits that will make it easier to save throughout your life.

Don't touch your retirement savings! The Wall Street Journal recently reported an increase in the number of individuals taking hardship withdrawals from their retirement savings.5 While you may not know when something might happen, you can be sure that at some point something financially unexpected will occur. Saving money for financial emergencies can be something you include in your budgeting plan each paycheck, but advisors suggest keeping it separate from your retirement savings.

Conclusion

As you begin to make decisions about jobs and careers, considering your retirement savings options can help you make informed choices. Ask questions and seek advice from a trusted professional to help you feel confident that you understand your options. Though retirement may feel a long way off, the more you begin to think about it and plan now, the more choices you will have later in your career when it comes to determining what you want your retirement to look like.

Notes

1 United States Department of Labor. "Top 10 Ways to Prepare for Retirement." September 2021, p. 1; https://www.dol.gov/sites/dolgov/files/ebsa/about-ebsa/our-activities/resource-center/publications/top-10-ways-to-prepare-for-retirement.pdf.

2 United States Bureau of Labor Statistics. Occupational Outlook Quarterly. Fall 2013, p. 16; https://www.bls.gov/careeroutlook/2013/fall/art02.pdf.

3 United States Bureau of Labor Statistics. See footnote 2.

4 Social Security Administration. "What Young Workers Should Know About Social Security and Saving." January 2009, p. 2; https://www.ssa.gov/newsletter/Statement%20Insert%2025+.pdf.

5 Tergesen, Anne. "Short on Cash, More Americans Tap 401(k) Savings for Emergencies." Wall Street Journal, February 2, 2023; https://www.wsj.com/articles/short-on-cash-more-americans-tap-401-k-savings-for-emergencies-11675305976.

© 2024, Federal Reserve Bank of St. Louis. The views expressed are those of the author(s) and do not necessarily reflect official positions of the Federal Reserve Bank of St. Louis or the Federal Reserve System.

Glossary

Defined-benefit retirement plan: A plan often funded by one's employer that promises a fixed, predetermined monthly benefit at retirement.

Defined-contribution retirement plan: A plan often managed and supported by one's employer that allows an individual to contribute to their own investment and/or savings account with potential earnings and/or tax benefits.

Mutual fund: An investment option that pools money from many investors and invests it in securities such as stocks, bonds, and short-term debt. Investors buy shares in mutual funds that represent their partial ownership in that fund and any resulting profits.

Roth retirement account: A type of savings account, such as a Roth individual retirement account (IRA) or Roth 401(k) account, that allows one to set aside after-tax income to be withdrawn tax free during retirement.

Social Security: A federal system of old-age, survivors', disability, and hospital care insurance that requires employers to withhold (or transfer) wages from employees' paychecks and deposit that money in designated accounts.

Traditional retirement account: A type of savings account, such as a traditional individual retirement account (IRA) or traditional 401(k) account, that allows one to set aside pre-tax income to lower taxable income now. Taxes are paid during retirement when the funds are withdrawn.