Individual Income Tax: The Basics and New Changes

"In this world nothing can be said to be certain, except death and taxes."

—Ben Franklin

Introduction

Taxes are certain. One primary tax is the individual income tax. Congress initiated the first federal income tax in 1862 to collect revenue for the expenses of the Civil War. The tax was eliminated in 1872. It made a short-lived comeback in 1894 but was ruled unconstitutional the very next year. Then, in 1913, the federal income tax resurfaced when the 16th Amendment to the Constitution gave Congress legal authority to tax income. And today, the federal income tax is well established and certain.

However, the details of income taxation are uncertain and subject to change. The 16th Amendment does not identify specific details. It does not define what portion of income should be taxed. It also does not define key elements of income tax such as tax deductions, tax exemptions, and expenses or how taxable income is determined. These omissions in the 16th Amendment allow federal income tax laws to change as lawmakers make decisions on raising revenue for government spending, making fairer tax laws, or stimulating the economy. And taxation laws have changed many times. The most recent change in tax laws came on December 22, 2017: President Trump signed the 2017 Tax Cuts and Jobs Act, which went into effect on January 1, 2018. But it's important to understand some basics of individual income taxation before these changes are addressed.

PART 1: The Basics

The Internal Revenue Service

Regardless of changes in taxation laws, taxes must be collected. In 1862, collection was the responsibility of a Commissioner of Internal Revenue. In 1894, this was changed to the Bureau of Internal Revenue and renamed in the 1950s as the Internal Revenue Service (IRS).1 The IRS is the branch of the Treasury Department responsible for implementing tax legislation, interpreting tax law, ensuring taxpayers' compliance with the law, and collecting income tax.

Additionally, for each new tax year there are hundreds of forms and publications the IRS updates and adjusts for the cost of living. Adjustments for inflation are beneficial to taxpayers and prevent credits or deductions from having a reduced value. These adjustments also prevent taxpayers from possibly paying a higher tax rate when there is no actual increase in real income. For example, if your income increases by 3 percent in a year when the inflation rate is also 3 percent, your real income hasn't changed. However, unless income tax brackets are adjusted each year for inflation, you might find yourself in a higher tax bracket (and thus paying a higher tax rate) even though in inflation-adjusted terms, your income hasn't changed. It's certain—the IRS is an important agency.

Collecting Income Tax

The Current Tax Payment Act was signed into law in 1943 and has made collecting income tax easier. This law requires employers to withhold federal income tax from an employee's paycheck each pay period and to send the payment directly to the IRS on behalf of the employee.2 In this way, income tax is collected on a pay-as-you-earn basis. The amount withheld is determined by information the employee provides on an IRS W-4 form. The information is used to calculate a reasonable estimate of the amount of income tax to be withheld from each paycheck.

By January 31 of each year, employers must furnish employees a W-2 Wage and Tax Statement. Employees use this form to complete individual tax returns. Among other things, it includes the total amount of income earned and the amount of federal tax withheld over the given year. Generally, if too much federal income tax has been withheld, a taxpayer will receive a refund. If not enough has been withheld, the taxpayer must pay the additional tax owed.

The Individual Taxpayer

Individual taxpayers are important for government funding. Individual income taxes are the leading source of revenue to support government spending. For example, in 2017, almost 48 percent of government revenue was provided by individual income tax (Figure 1).

Taxable Income

All individuals who meet certain income requirements must file an annual tax return—it's the law. Taxpayers must identify all forms of income and calculate the amount of taxable income to arrive at their tax liability. Taxable income is calculated based on the taxpayer's adjusted gross income for the tax year minus allowable tax exemptions, deductions, and credits. But changes in taxation laws change the details and can make filing a tax return complicated.

Filing Status and Tax Brackets

When filing a return, a taxpayer's filing status is classified as married or unmarried. Married taxpayers can choose to either combine their incomes and file a joint return or file separately. Unmarried taxpayers are classified as either single taxpayers or heads of household if they meet certain guidelines. There is also an additional qualifying widow(er) status for those who meet special circumstances. These taxpayers are allowed to use the joint return tax rates.

After calculating taxable income and identifying a filing status, the amount of tax liability can be determined using percentage rates. Taxable income is divided into brackets that group income according to amounts. Income within each bracket is taxed at a specific rate for that bracket. Income limits in each bracket are different for each filing status. This process ensures the federal individual income tax is a progressive tax based on the ability-to-pay principle. This progressive tax applies higher tax rates to higher income brackets than those applied to lower brackets. While that might seem complicated, the structure ensures that taxpayers with lower incomes pay a smaller overall tax rate than those with higher incomes.

The tax bracket system uses marginal tax rates when income falls into different brackets. Here, the word "marginal" means additional. The first dollars earned fall into the first bracket, which is taxed at the lowest rate. When income "fills" that bracket, additional dollar amounts get bumped into the next bracket and taxed at a higher rate. This process continues until all of a taxpayer's taxable income is accounted for and included in a bracket. So, individual tax payers might pay taxes in several different brackets depending on their income because the money that falls in each tax bracket is taxed at a different rate. (Once the amount of tax owed is calculated, it can be divided back into total income to determine the average tax rate for an individual taxpayer.)

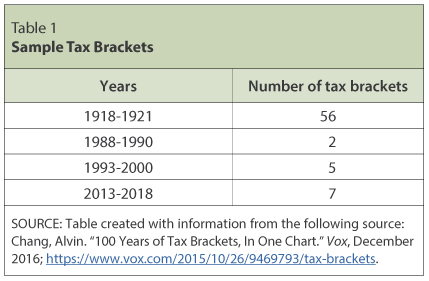

Notice that there are two important factors here: the tax bracket and the tax percentage rate. A greater number of tax brackets with increasingly higher tax rates guarantees a more progressive tax structure. Fewer brackets result in a wider range of incomes being taxed at the same percentage rate and a less progressive structure. The number of tax brackets has varied greatly from year to year according to changes in taxation laws.3 (See examples in Table 1.)

Tax Rates

Throughout the years, the tax percentage rates have varied greatly within tax brackets to support legislative actions and government expenditures (Figure 2). For example, the extreme increase in percentage rates for top income earners changed in 1917 to support World War I. A large percentage increase was also seen in 1944 because of World War II. Will Rogers lived during this time period, and his words reflect his humorous outlook on tax changes: "The difference between death and taxes is death doesn't get worse every time Congress meets."4

The taxable income limits in each tax bracket change as well as the tax percentage rate for each bracket. For example, in 1913, the top tax bracket had a 7 percent rate on all taxable income over $500,000.5 In 2018, the top tax bracket has a 37 percent rate on all taxable income over $600,000. These income limits may be changed for a specific purpose or adjusted for cost-of-living expenses to minimize the effect of inflation.

Equally important to the tax brackets and tax rates are refundable credits such as the Earned Income Tax Credit (EITC) and the Additional Child Tax Credit. These two tax credits, designed to provide tax relief for low- to middle-income earners, are based on a taxpayer's taxable income and number of children. Refundable tax credits are different from regular tax credits. They not only reduce the amount of taxes owed or completely eliminate any taxes owed but can result in a refund as well. When refundable tax credits reduce the tax liability to below zero, a refund is given for the difference. In 2017, more than 15.5 million tax refunds included a refundable child tax credit, and more than 23.3 million included a refundable earned income tax credit.6

PART 2: New Changes

The 2017 Tax Cuts and Jobs Act

The most recent change in taxation laws, the 2017 Tax Cuts and Jobs Act, includes many changes effective for 2018. The combined impact affects each taxpayer differently. Some basic changes are addressed as follows:

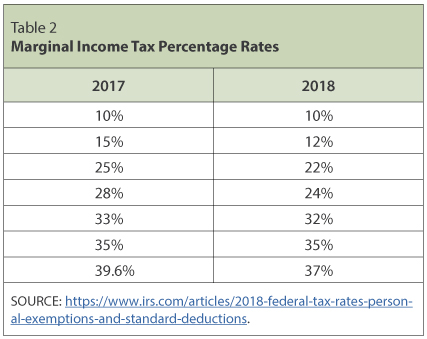

1. There are new tax rates within brackets. The number of tax brackets has not changed from 2017 and remains at seven tax brackets. However, in 2018, the rates have decreased overall (Table 2).

In any tax year, moving into a higher tax bracket does not mean that all of your taxable income will be taxed at a higher rate. Instead, only the income that you earn within a particular bracket is subject to that particular tax rate.

Example: For 2018, the income tax of a single taxpayer with a taxable income of $40,000 is calculated based on the first three brackets (see "2018 Income Tax Brackets").

Bracket 1: The first $9,525 of taxable income is taxed at 10 percent. [10% × $9,525.00 = $952.50 tax on this portion of taxable income]

Bracket 2: Taxable income from $9,526 to $38,700 is taxed at 12 percent ($38,700 – $9,525 = $29,175). [12% × $29,175.00 = $3,501.00 tax on this portion of taxable income]

Bracket 3: Taxable income from $38,701 to $40,000 is taxed at 22 percent ($40,000 – $38,700 = $1,300). [22% × $1,300.00 = $286.00 tax on this portion of taxable income]

Total tax liability: $952.50 + $3,501.00 + $286.00 = $4,739.50

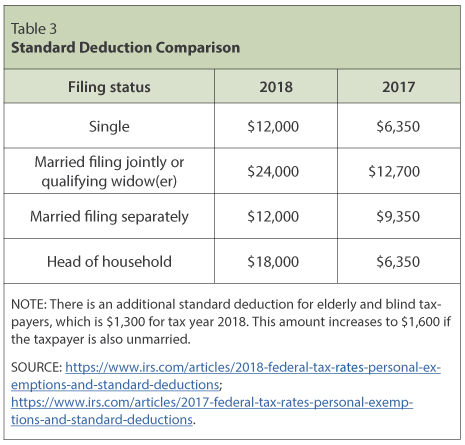

2. The standard deduction has increased. The standard deduction is subtracted from adjusted gross income and reduces taxable income. Taxpayers can choose to take the higher of either the standard deduction or their itemized deductions—whichever results in the lowest tax. This increased standard deduction means more taxpayers will benefit by taking the standard deduction beginning in 2018 (Table 3).

3. In 2017, the Child Tax Credit was a nonrefundable credit of up to $1,000 per qualifying child for taxpayers with earned income of at least $3,000. This means it did not reduce tax liability below zero dollars. When this credit was more than the amount of tax owed, a taxpayer might have been eligible to claim the unused amount of the credit by filing for the Additional Child Tax Credit—a refundable credit.7 The beginning phase-out income limit for married taxpayers filing jointly was $110,000 in 2017.8

Under the 2017 Tax Cuts and Jobs Act, the Child Tax Credit and the Additional Child Tax Credit have been combined with the following new guidelines and changes effective for 20189:

- The Child Tax Credit has increased to $2,000 for each qualifying child.

- There is a refundable portion of the credit, limited to $1,400.

- The earned income threshold for the refundable credit is lowered to $2,500.

- The phase-out income limits for the child tax credit increases in 2018 to $200,000 ($400,000 for joint filers).

4. The limit on charitable contributions of cash has increased from 50 percent to 60 percent of adjusted gross income.

5. Some deductions have been reduced or eliminated, including the following examples10:

- The deduction of state and local income, sales, and property taxes is limited to a combined, total deduction of $10,000 (or less depending on filing status).

- Some miscellaneous expenses are limited or are no longer deductible. Examples include deductions for employee business expenses, tax preparation fees, job search expenses, and safe deposit box fees.11

- Moving expenses are no longer deductible.

- Personal exemptions have been eliminated. For reference, in 2017 the exemption amount was up to $4,050 per qualifying person.

6. The EITC remains in effect in the new tax law with new guidelines and adjustments for inflation and cost-of-living allowances. The EITC allows taxpayers to get a refund, even if they do not owe or have not paid any tax. To qualify for this credit, certain requirements must be met that depend on income level, filing status, and number of qualifying children. Also, a tax return must be filed to claim the credit. For 2018, the maximum EITC amount available is $6,431 for taxpayers filing jointly who have three or more qualifying children.12 In 2017, almost 27 million taxpayers received over $65 billion from the EITC.13

7. One very noticeable change from the 2017 Tax Cuts and Jobs Act is the new Form 1040, which will simplify filing for many taxpayers. It is about half the size of the old version and consolidates the older Form 1040, Form 1040A, and Form 1040EZ all into one form. The streamlined form can be supplemented with additional schedules as needed for more complex tax situations.14

Conclusion

Our nation's first income tax was signed into law by President Lincoln in 1862. It levied a 3 percent tax on incomes between $600 and $10,000 and a 5 percent tax on incomes of more than $10,000.15 And in 1913, the first Form 1040 appeared after Congress levied a 1 percent tax on net personal incomes above $3,000 and a 6 percent tax on incomes of more than $500,000.16 These historical taxation laws bear little resemblance to the most recent change in taxation laws, the 2017 Tax Cuts and Jobs Act passed by Congress and signed into law by President Trump. Many factors such as inflation, employment, workforce changes, and adjustments to the federal budget contribute to tax law changes. And with each change, taxpayers are affected.

History shows that income tax law is always changing. Ben Franklin died in 1790—many years before the first federal income tax was levied. But his words have outlived him: "In this world nothing can be said to be certain, except death and taxes." What Franklin did not address was the uncertainty of change in taxation laws. Regardless of the intent, change can bring confusion. Having an understanding of taxation laws in one time period does not guarantee understanding of new taxation laws. With the ever-changing taxation laws, more than 9 out of 10 taxpayers use software or a tax preparer to complete and file their tax returns17—because changing tax laws can be complex.

Notes

1 IRS. "Brief History of IRS." Accessed October 8, 2018; https://www.irs.gov/uac/brief-history-of-irs.

2 Tax History.com. "Historical Perspectives on the Federal Income Tax." Accessed October 17, 2016; http://www.taxhistory.com/1943.htm.

3 Chang, Alvin. "100 Years of Tax Brackets, In One Chart." Vox, December 2016; https://www.vox.com/2015/10/26/9469793/tax-brackets.

4 Will Rogers. AZQuotes.com, Wind and Fly LTD, 2018. Accessed October 10, 2018; https://www.azquotes.com/quote/249398.

5 Bradford Tax Institute. "History of Federal Income Tax Rates: 1913-2018"; https://bradfordtaxinstitute.com/Free_Resources/Federal-Income-Tax-Rates.aspx.

6 IRS. Internal Revenue Service Data Book, 2017. Publication 55B. Washington, DC: March 2018, p. 2; https://www.irs.gov/pub/irs-soi/17databk.pdf.

7 IRS. "The Additional Child Tax Credit: A Refundable Tax Credit for Parents." Accessed October 2018; https://www.irs.com/articles/additional-child-tax-credit.

8 Bird, Beverly. "The Child Tax Credit: 2017 vs. 2018." Balance, August 2018; https://www.thebalance.com/child-tax-credit-changes-4158690.

9 Charney, Gil. "The New Child Tax Credit." H&R Block, October 2018; https://www.hrblock.com/tax-center/irs/tax-reform/new-child-tax-credit/.

10 IRS. "Steps to Take Now to Get a Jump on Next Year's Taxes." 2018; https://www.irs.gov/individuals/steps-to-take-now-to-get-a-jump-on-next-years-taxes.

11 IRS. "Tax Reform Provisions that Affect Individuals." 2018; https://www.irs.gov/newsroom/individuals.

12 IRS. "2018 EITC Income Limits, Maximum Credit Amounts and Tax Law Updates." 2018; https://www.irs.gov/credits-deductions/individuals/earned-income-tax-credit/eitc-income-limits-maximum-credit-amounts-next-year.

13 IRS. "Qualifying for the Earned Income Tax Credit." 2018; https://www.irs.gov/newsroom/qualifying-for-the-earned-income-tax-credit.

14 IRS. "Working on a New Form 1040 for 2019 Tax Season." IR-2018-146, June 29, 2018; https://www.irs.gov/newsroom/irs-working-on-a-new-form-1040-for-2019-tax-season.

15 IRS. "Historical Fact of the IRS"; https://www.irs.gov/newsroom/historical-highlights-of-the-irs.

16 IRS. "Brief History of IRS." Accessed October 8, 2018; https://www.irs.gov/uac/brief-history-of-irs.

17 IRS. "Working on a New Form 1040 for 2019 Tax Season." IR-2018-146, June 29, 2018; https://www.irs.gov/newsroom/irs-working-on-a-new-form-1040-for-2019-tax-season.

© 2018, Federal Reserve Bank of St. Louis. The views expressed are those of the author(s) and do not necessarily reflect official positions of the Federal Reserve Bank of St. Louis or the Federal Reserve System.

Glossary

Adjusted gross income: Gross income minus specific adjustments to income. (Gross income is the total amount earned before any adjustments are subtracted.)

Earned income: Money you get for the work you do. There are two ways to get earned income: You work for someone who pays you, or you own or run a business or farm.

Income: The payment people receive for providing resources in the marketplace. When people work, they provide human resources (labor) and in exchange they receive income in the form of wages or salaries. People also earn income in the form of rent, profit, and interest.

Income tax: Taxes on income, both earned (salaries, wages, tips, commissions) and unearned (interest, dividends). Income taxes can be levied on both individuals (personal income taxes) and businesses (business and corporate income taxes).

Inflation: A general, sustained upward movement of prices for goods and services in an economy.

Revenue (government): The income received by government from taxes and other sources.

Taxable income: Adjusted gross income minus allowable tax exemptions, deductions, and credits; the amount of income that is subject to income tax.

Tax credit: An amount directly deducted from the total tax owed.

Tax deduction: Allowable expenses defined by tax law that can be subtracted from adjusted gross income to reduce taxable income.

Taxes: Fees charged on business and individual income, activities, property, or products by governments. People are required to pay taxes.

Tax exemption: An amount allowed by the IRS that can be deducted from taxable income to reduce the amount of income tax owed.