Credit Bureaus: The Record Keepers

"Creditors have better memories than debtors."

—Benjamin Franklin

Introduction

If you've taken a personal finance class, listened to the news on radio or television, read articles in the newspaper, or participated in social media, chances are you've seen or heard something about a credit bureau. In fact, the term "credit bureau" is so commonly mentioned that you may have not given much thought to the work and power of credit bureaus and how this affects you. Actually, there is much to learn about credit bureaus—and the records they keep.

What Is a Credit Bureau?

A credit bureau can be defined by considering the meaning of the two separate words. The root word of "credit"—cred—means "believe." Credit is based on the belief that borrowed money will be paid back. As used here, "bureau" means an office or department that collects and distributes information. The two words together mean a business that collects and distributes information about individuals and businesses to lenders. Decisions on granting credit are based on belief established by credit records. In the words of the American businessman and author Robert Kiyosaki, "Credit is another word for trustworthiness." Credit bureaus provide reports that help to establish trustworthiness.

Credit bureaus, also known as credit reporting agencies or consumer reporting agencies, are for-profit businesses. Collectively, they earn approximately $4 billion annually.1 They collect, store, and update credit information on most consumers and then sell the information to lenders such as banks, mortgage lenders, credit card companies, and other financing companies. Bureaus compete for this market by providing accurate information to lenders at a competitive price.

Additionally, credit bureaus sell data in different ways. For example, a common practice is to sell lenders lists of consumers who meet predefined criteria for pre-approved offers. In general, these offers may allow consumers to receive credit or loans quickly. Credit bureaus also sell services directly to consumers, such as credit monitoring and fraud and identity theft protection.

Why, How, and When Credit Bureaus Started

Credit bureaus first emerged in the United States in the late 1800s to help lenders.2 At that time, merchants depended on their personal knowledge about customers. Extending credit was very risky. A consumer could default on a debt and simply go get credit somewhere else. To prevent losses, local merchants started keeping records on "bad customers" who didn't pay their credit satisfactorily and were a poor credit risk.3

Over time, the need to know customer credit worthiness increased. "Good customer" lists were developed and shared for a price. Lenders paid for such lists and used them to determine who would be given credit. The practice gradually expanded into for-profit companies.4

Beginning in the 1920s with the introduction of retail installment credit and continuing to the 1950s with the introduction of revolving credit accounts, credit reporting became increasingly important to both lenders and borrowers. As the demand for credit reporting increased, credit reporting companies began consolidating.5

The modern credit reporting industry began in the 1960s when computers made data collection and sharing faster and easier. By the 1970s, practically all credit data were on computers. And beginning in the late 1980s, the internet added a new dimension—data collection and credit reporting online.6

The Big Three

Today there are three major national credit bureaus in the United States: Experian, Equifax, and TransUnion. Each of these "Big Three" maintains credit files on more than 200,000,000 Americans.7 In addition, each bureau has developed a particular focus: Experian specializes in providing marketing services to businesses, for example for pre-approved credit card offers. Equifax works closely with corporate credit analysis. TransUnion specializes in analyzing credit information on Americans living abroad.8

The Big Three, however, are not the only credit reporting agencies. Over 400 smaller, regional, or industry-specific credit bureaus exist in the United States.9 They collect and share information with creditors and other businesses that need specific information such as rental, medical, or employment histories.10 All credit bureaus operate independently of each other and generally do not share collected information with each other.

Gathering Credit Information

Every year, credit bureaus collectively make over 36 billion updates to consumer files from data from about 18,000 sources.11 The data come from creditors who do business with consumers—for example, banks, credit card issuers, retailers, and auto finance companies (see Figure 1). Permission to share credit information, including with credit bureaus, is generally granted when a consumer signs up for credit. For credit cards, for example, the specifics are usually explained in the fine print of the disclosure agreement (see the boxed insert "Sample Credit Card Customer Agreement"). Credit bureaus also gather information from public records, such as those for tax liens, bankruptcies, and court judgements and proceedings.12

Figure 1

Where Do the Big Three Credit Bureaus Get Information?

SOURCE: CFPB. "CFPB Report Details How the Nation's Largest Credit Bureaus Manage Consumer Data." December 13, 2012; https://www.consumerfinance.gov/about-us/newsroom/consumer-financial-protection-bureau-report-details-how-the-nations-largest-credit-bureaus-manage-consumer-data/.

Reporting Information

Lenders submit both positive and negative information electronically each month to at least one of the three major credit bureaus. They do not necessarily report to all three, and they do not all report at the same time. Consequently, one credit bureau may have more current information than another.

Although lenders furnish data to credit bureaus voluntarily, there are incentives for reporting. First, lenders need accurate and complete records to determine future credit decisions. As noted by the Federal Reserve Board, "for the full benefits of the credit-reporting system to be realized, credit records must be reasonable, complete, and accurate."13 Second, reporting encourages timely payments from borrowers. Consumers are more likely to repay debts when they know a creditor may report late payments or delinquent accounts, which can hinder their ability to obtain credit in the future. Finally, when consumers repay debt on time, their credit is positively impacted, which builds a larger pool of trustworthy borrowers for future business. On the other hand, there are disincentives for creditors to report borrower information to credit bureaus. For example, credit bureaus may sell the names of creditworthy borrowers to competing lenders who then compete for those same customers.14

Credit Reports

The credit bureaus each individually maintain the credit history of an individual in a credit report. It is estimated that credit bureaus release 3 billion credit reports annually.15 Individuals can request their own credit reports. Additionally, businesses with a legally valid need to view credit information can request credit reports. For example, when you apply for a credit card, the credit card company has a valid need to look at your credit information. Your information is also sold to companies that may prescreen you for their products and services.

Credit reports determine if you are eligible for credit and how much you have to pay for it. The reports can also influence your opportunity to get a job, rent or buy a house, or even buy insurance. A credit report includes the following information16:

- Personal data: Name, birth date, Social Security number, past and current addresses, phone numbers, and employers

- Accounts: Revolving credit accounts and installment loans, including creditor names, account numbers, amounts owed, payment histories, and whether any account is past due

- Public records: Court judgments, bankruptcies, and tax liens

- Recent inquiries: Who has recently viewed your credit report

Negative information on a credit report does not remain on a report forever. Information about a lawsuit or a judgment against a consumer may be reported for seven years or until the statute of limitations runs out, whichever is longer. Bankruptcies may be reported for up to 10 years, and unpaid tax liens may be reported for 15 years.17 As of July 2017, tax liens and civil debts will be excluded from credit reports if they do not include a consumer's name, address, and either a Social Security number or date of birth.18

Credit Scores

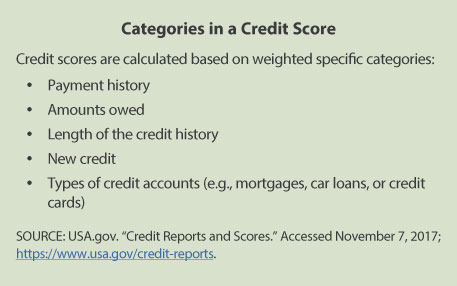

A credit score is a three-digit number based on information in a credit report. Credit scores are calculated at the time requested and are not stored as part of a credit report. Credit scores indicate a person's credit risk (see the boxed insert "Categories in a Credit Score").

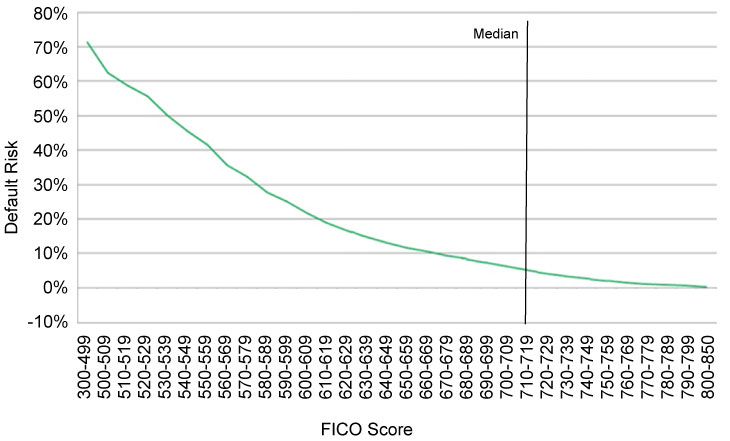

Lenders use credit scores to decide whether to offer credit and the interest rate a person pays. Although there are different scores and models, the FICO® credit score is the most widely used score. FICO stands for Fair Isaac Corp., the company that developed the FICO credit-scoring model. Lenders rely on FICO scores as an indicator of responsible financial behavior. Higher FICO scores indicate a lower risk of default on credit; that is, consumers with a high FICO score tend to make payments on time and use credit responsibly. Conversely, lower credit scores indicate a higher default credit risk; that is, consumers with a lower FICO score tend to make late and/or no payments (see Figure 2).

Figure 2

Default Risk by FICO Score

SOURCE: CFPB. "Analysis of Differences between Consumer- and Creditor-Purchased Credit Scores." September 2012, p. 10; http://files.consumerfinance.gov/f/201209_Analysis_Differences_Consumer_Credit.pdf.

Regulation

The first federal law regulating credit bureaus was the Fair Credit Reporting Act enacted in 1971. This act has been revised numerous times, including by the Fair and Accurate Credit Transactions Act of 2003 (FACT Act). The FACT Act created new responsibilities for credit reporting agencies and users of credit reports, many concerning credit disclosures and identity theft. It also created new rights for consumers, including the right to free annual credit reports (see the boxed insert "Check Your Credit Reports").19

In 2012, the Consumer Financial Protection Bureau (CFPB) became the first federal agency to supervise all aspects of the credit reporting market.20 The CFPB works to ensure consumer financial products and services are fair by implementing and enforcing consumer financial laws.21

Additionally, the Federal Trade Commission (FTC) is an independent agency of the U.S. federal government designed for consumer protection to prevent fraudulent, deceptive, and unfair business practices and to provide information to identify and avoid them. By law, the CFPB and the FTC are required to work together to "coordinate their enforcement activities and promote consistent regulatory treatment of consumer financial products and services."22

Conclusion

The primary purpose of credit bureaus is record keeping. They collect information on consumers who use credit and charge a fee to issue credit reports. Creditors pay for these reports and use them when making decisions about extending credit and the terms of credit offered. Credit records may provide insight into future behavior23 and reflect the belief that a person's ability to repay a debt is directly related to how they have handled debt in the past. A review of a consumer's credit reports can reduce the risk of lending.

Credit reports can benefit consumers, too. Credit reports reflect the financial behavior of individuals, and for those who are financially responsible, there is a big reward: credit with favorable terms. Most consumers cannot afford to pay cash for a house, car, or other large purchases and depend on credit—made available with good credit records. Having a record that shows financial responsibility includes many things such as paying bills on time and managing debt. Credit reports can also serve to protect consumers from making purchases they can't afford. As the late U.S. Secretary of Commerce Jesse H. Jones once said, "One of the greatest disservices you can do a man is to lend him money that he can't pay back."

Notes

1 Consumer Financial Protection Bureau (CFPB). "Fact Sheet: Credit Reporting Market." Accessed November 7, 2017; http://files.consumerfinance.gov/f/201207_cfpb_factsheet_credit-reporting-market.pdf.

2 CFPB. "Key Dimensions and Processes in the U.S. Credit Reporting System: A Review of How the Nation's Largest Credit Bureaus Manage Consumer Data." December 2012, p. 7; http://files.consumerfinance.gov/f/201212_cfpb_credit-reporting-white-paper.pdf.

3 CreditRepair.com. "What Is a Credit Bureau? Know Their History." Accessed November 7, 2017; https://www.creditrepair.com/articles/credit-improvement/history-of-credit-bureaus.

4 Rotter, Kimberly. "Credit Bureau Guide: What the Differences Are Between Equifax, TransUnion, & Experian." July 5, 2016; https://www.creditsesame.com/blog/credit/credit-bureau-guide-what-the-differences-are-between-equifax-transunion-experian/.

5 See footnote 2.

6 Rotter, Kimberly. "A History of the Three Credit Bureaus." Accessed November 7, 2017; https://www.creditrepair.com/blog/credit/credit-bureau-history/.

7 See footnote 1.

8 See footnote 6.

9 See footnote 7.

10 Stone, Corey. "So How Many Consumer Reporting Companies Are There?" CFPB, July 16, 2012; https://www.consumerfinance.gov/about-us/blog/so-how-many-consumer-reporting-companies-are-there/.

11 Consumer Data Industry Association. Statement of Stuart K. Pratt before the Committee on Financial Services, Subcommittee on Financial Institutions and Consumer Credit. House of Representatives, March 24, 2010, p. 7; https://web.archive.org/web/20100409163529/http://www.house.gov/apps/list/hearing/financialsvcs_dem/pratt_testimony.pdf.

12 Board of Governors of the Federal Reserve System. "Credit Reports and Credit Scores." Accessed November 7, 2017; https://www.federalreserve.gov/creditreports/pdf/credit_reports_scores_2.pdf.

13 Board of Governors of the Federal Reserve System. "Report to Congress on Credit Scoring and Its Effects on the Availability and Affordability of Credit." August 2007, p.17; http://www.federalreserve.gov/boarddocs/rptcongress/creditscore/creditscore.pdf.

14 See footnote 2.

15 See footnote 7.

16 Experian. "Credit Report Basics." Accessed November 7, 2017; https://www.experian.com/blogs/ask-experian/credit-education/report-basics/.

17 USA.gov. "Credit Reports and Scores." Accessed November 7, 2017; https://www.usa.gov/credit-reports.

18 McCoy, Kevin. "Consumer Credit Scores to Exclude Some Debts, Liens Starting July 1." USA TODAY, March 2017; https://www.usatoday.com/story/money/2017/03/13/reports-credit-scores-soon-exclude-some-debts-liens/99113572/.

19 Board of Governors of the Federal Reserve System. "Fair Credit Reporting" in Consumer Compliance Handbook. June 2011, p. 1; https://www.federalreserve.gov/boarddocs/supmanual/cch/fcra.pdf.

20 CFPB. "CFPB Oversight Uncovers and Corrects Credit Reporting Problems." March 2, 2017; https://www.consumerfinance.gov/about-us/newsroom/cfpb-oversight-uncovers-and-corrects-credit-reporting-problems/.

21 CFPB. "Rulemaking." Accessed November 7, 2017; https://www.consumerfinance.gov/policy-compliance/rulemaking/.

22 FTC. "Federal Trade Commission, Consumer Financial Protection Bureau Pledge to Work Together to Protect Consumers." January 23, 2012; https://www.ftc.gov/news-events/press-releases/2012/01/federal-trade-commission-consumer-financial-protection-bureau.

23 Excluding consumers who have a low credit score or no score at all because they don't use credit.

© 2017, Federal Reserve Bank of St. Louis. The views expressed are those of the author(s) and do not necessarily reflect official positions of the Federal Reserve Bank of St. Louis or the Federal Reserve System.

Glossary

Bankruptcy: A legal process for declaring that a person is unable to pay his or her debts. The process may involve a court- supervised process of selling the bankrupt person's belongings to pay part of the debts owed to creditors.

Credit card: A card that represents an agreement between a lender—the institution issuing the card—and the cardholder. Credit cards may be used repeatedly to buy products or services or to borrow money, which must be repaid with interest.

Creditor: A person, financial institution, or other business that lends money.

Debt: Money owed in exchange for loans or for goods or services purchased with credit.

Identity theft: A form of stealing that results in someone gaining access to another person's personal information (name, credit card numbers, date of birth, etc.) to commit crimes (steal money, open a credit card, etc.).

Installment credit: A loan given in a lump sum for a specific purchase or investment. The loan is paid back with regularly scheduled payments, which include interest. Examples include home loans, car loans, and business loans.

Lender: An individual or organization that provides money to a borrower with the expectation that the borrower will pay the money back.

Mortgage: A loan for the purchase of a home or real estate.

Revolving credit: A line of available credit that is usually designed to be used repeatedly, with a preapproved credit limit. The amount of available credit decreases and increases as funds are borrowed and then repaid with interest.