Bankruptcy: When All Else Fails

"Bankruptcy is about financial death and financial rebirth. Bankruptcy is the great American story rewritten." 1

—Elizabeth Warren, U.S. Senator

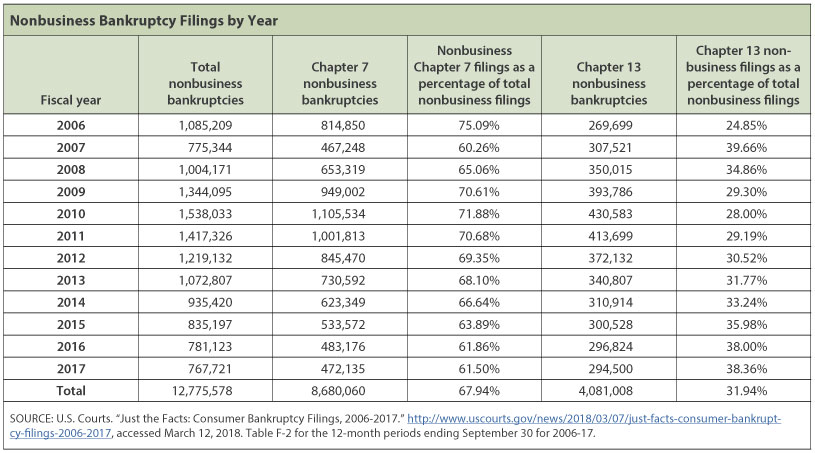

Not overspending can help life go more smoothly. Still, many people find themselves in financial trouble. In fact, there were approximately 800,000 bankruptcies filed in 2017 (see the table for a breakdown of bankruptcy filings).2 Hopefully you will never find yourself unable to pay your debts, but it is good to know there are options available should you need serious financial help.

Personal Finance Basics

First Things First—Earning Income

When it comes to money and being prepared, it is important to mention personal income. Earning income results from the skills you develop and apply to your work; this is what economists call human capital. Typically, the more skills you develop and the higher education level you attain, the higher income you will earn and the lower unemployment you will face.3 Of course, this also depends on what you study and the job market.

Budgets

Once you are earning income, developing a budget is a powerful tool you can use to help keep your finances in order. A budget is an itemized summary of estimated income and expenses for a given period, usually monthly. Budgeting can help you set goals, plan for major purchases, and make cutbacks in spending when necessary so that you can cover any unexpected expenses.

When Financial Problems Happen

Having a budget can help you establish good personal finance habits, such as saving part of your income and paying bills on time. Unfortunately, whether living within a budget or not, people can find themselves in difficult financial circumstances. There are many reasons for financial problems; sometimes the problems are temporary, minor setbacks, such as needing a new laptop because of damage that cannot be repaired. Other times, people experience long-lasting, catastrophic financial situations, such as when they incur large medical bills from a traffic accident and cannot go back to work.

Late Payments

Financial trouble often has a way of catching people when they least expect it. Little things like birthday gifts and spending money for vacation can impact a person's budget, but bigger issues like car repairs, medical expenses, and an inability to work can be very hard and sometimes impossible to navigate. Sometimes paying your bills late may not be your fault. For example, if you owned a business and were waiting for a client to pay for services you had provided, you could find yourself affected by that person's slow payment. If you did not have adequate savings to cover your expenses while waiting for payment, you could fall behind on your own payments. Regardless of whether late payments are your fault, they can have negative consequences, including late fees added to the amount already owed. In addition, depending on how late the payments are, there can be negative effects on a person's credit score. A person's payment history and credit score are listed on a credit report. A credit report lists all the credit activity a person has had and how well they have paid back the money owed.4 This is similar to the list of classes and grades found on a transcript. A credit score is a number based on information in a credit report, which indicates a person's credit risk. A low credit score means it will be more difficult to obtain credit, just like a low grade point average on a transcript makes it more difficult to be accepted into technical college or a university.

There are different types of financial trouble, with credit card debt being the most common. If you find yourself unable to make one or two payments, it is best to contact the individual creditor or credit card company, try to explain the situation, and make arrangements with them to pay. This may increase your interest rate and may also affect your credit score. Ignoring or avoiding a creditor's calls will not make the situation better, nor will the issue go away. Creditors are in business to make money, and your late payments affect their ability to pay their own creditors. When creditors do not receive payments on time, based on the contract you signed when you obtained the credit, they may use legal action to collect the money you owe.

Collections

If you have not been making payments and have not made arrangements with your creditors, they will likely turn your accounts over to a debt collection agency. A collection agency will contact you and attempt to get you to pay back the money. Debt collection agencies are highly regulated by the Federal Trade Commission to enforce ethical and legal collection practices.5 It is best to avoid paying any debt late if at all possible. Unfortunately, even with the best intentions, a good plan, and the use of a budget, people can still find themselves with debt so large that they can never pay their creditors back while maintaining a basic standard of living and avoiding hardship. When people have exhausted all of their usual options and are still unable to pay their debt, they have the option of legal protection in the form of bankruptcy. Of course, there are various reasons for bankruptcy, including medical expenses, loss of a job, excessive or unwise use of credit, separation or divorce, and unexpected expenses (e.g., natural disasters).

Filing a Bankruptcy Case

Bankruptcy can offer debtors—persons or organization that owe an amount of money—some protection from creditors under federal law while they review their situation and options. A fundamental goal of the federal bankruptcy laws enacted by Congress is to give debtors a "fresh start." The Supreme Court made this point in a 1934 decision: "[I]t gives to the honest but unfortunate debtor…a new opportunity in life and a clear field for future effort, unhampered by the pressure and discouragement of preexisting debt."6

A bankruptcy case is a federal civil case with specialized laws. It is where a bankruptcy judge determines how a debtor's money and assets should be distributed among his or her creditors. The consequences and complexities of filing for bankruptcy are significant and require careful consideration and advice—usually from an experienced bankruptcy attorney. The minute a debtor files bankruptcy, an automatic stay goes into effect. The automatic stay is an injunction intended to stop all actions by creditors and debt collection agencies to collect debts. This does not always happen, however, as sometimes it takes an action by the debtor's attorney or a lawsuit to stop some collection agencies. There are various types, or chapters, of bankruptcy; two common types that individuals file are Chapter 7 and Chapter 13.

A Chapter 7 bankruptcy case is a liquidation case. A trustee is appointed to take over a debtor's property. Any property of value may be sold or turned into money to pay creditors. Some personal items and possibly real estate, depending on state laws where the debtor lives, can be retained by the debtor as exempt from collection. After any non-exempt assets have been distributed to creditors, any remaining debt, with some exceptions, is discharged and the debtor will never have to repay those debts. The discharge is a permanent court order prohibiting the creditors that the debtor named in the bankruptcy documents from taking any form of collection action on discharged debts. This includes legal action and communications such as telephone calls, letters, or any personal contact. The debts that cannot be discharged include nearly all taxes, student loans, child support, and alimony (payments to a former spouse); court fines and criminal restitution; and personal injury caused by driving drunk or driving under the influence of drugs.7

People filing for Chapter 13 can usually keep their property, but there are conditions. To be eligible for a Chapter 13 case, the debtor must have some kind of regular income. The bankruptcy court must approve a repayment plan and budget that can last for a period of up to 60 months. The repayment plan allows the debtor to pay a percentage of debts during the life of the plan. A trustee is appointed and will collect monthly payments from the debtor, pay creditors, and make sure the terms of the repayment plan are current. If all the payments are made under the plan, then some debts will have been paid in full, while the remainder of other debts, such as credit card debts, will be discharged.

Consequences of Bankruptcy

Choosing to file bankruptcy should not be taken lightly. It is a serious decision with lasting consequences. For example, bankruptcy can remain on your credit report for up to 10 years, which will affect your ability to obtain credit and get a lower interest rate.8 Filing bankruptcy can also affect your ability to obtain employment or choose where to live. Employers, especially banks, financial service providers, certain IT companies, and government agencies that require security clearances often run credit checks on job applicants before making an offer of employment, and they'll check their current employees' credit as well. Banks and mortgage brokers always obtain credit reports, which can affect the amount you are able to borrow, and this can affect the neighborhood in which you can afford to buy a home.

Conclusion

For most people, bankruptcy should be avoided. Reducing the possibility of bankruptcy starts with good financial preparation. Preparation includes developing your human capital to earn a higher income, establishing and living on your budget, saving money, and paying your bills on time. If disaster strikes, it is important to know that bankruptcy is an option, albeit a last resort.

A special thanks to Shaun K. Stuart, an attorney advisor at the Bankruptcy Clerk's Office, Missouri Eastern Bankruptcy Court, St. Louis, for her assistance with this article.

Notes

1 Warren, Elizabeth. Frontline interview, September 20, 2004; https://www.pbs.org/wgbh/pages/frontline/shows/credit/interviews/warren.html, accessed March 1, 2018.

2 U.S. Courts; http://www.uscourts.gov/statistics/table/f/bankruptcy-filings/2017/12/31, accessed March 5, 2018.

3 U.S. Department of Labor, Bureau of Labor Statistics, Employment Projections; https://www.bls.gov/emp/ep_chart_001.htm, accessed March 5, 2018.

4 Federal Trade Commission. "Credit and Your Consumer Rights." https://www.consumer.ftc.gov/articles/pdf-0070-credit-and-your-consumer-rights, accessed March 1, 2018.

5 Federal Trade Commission. "Debt Collection." https://www.ftc.gov/news-events/media-resources/consumer-finance/debt-collection, accessed March 1, 2018.

6 Local Loan Co. v. Hunt, 292 U.S. 234, 244 (1934).

7 11 U.S.C. §§ 523 and 727.

8 Federal Trade Commission (2018, see footnote 4).

© 2018, Federal Reserve Bank of St. Louis. The views expressed are those of the author(s) and do not necessarily reflect official positions of the Federal Reserve Bank of St. Louis or the Federal Reserve System.

Glossary

Bankruptcy: A legal process for declaring that a person is unable to pay his or her debts. The process may involve a court-supervised process of selling the bankrupt person's belongings to pay part of the debts owed to creditors.

Budget: An itemized summary of estimated income and expenses for a given period. A budget is a plan for managing income, spending, and saving during a given period of time.

Contract: An exchange, promise, or agreement between two parties that is enforceable by law. For example, a car buyer agrees to pay the amount financed at an agreed-upon interest rate for the length of the contract.

Credit report: A loan and bill payment history kept by a credit bureau and used by financial institutions and other potential creditors to determine the likelihood that a future debt will be repaid.

Credit score: A number based on information in a credit report, which indicates a person's credit risk.

Debtor: A person or organization that owes an amount of money.

Human capital: The knowledge and skills that people obtain through education, experience, and training.