Education, Income, and Wealth

"By some estimates, income and wealth are near their highest levels in the past hundred years, much higher than the average during that time span and probably higher than for much of American history before then."

—Janet Yellen, Federal Reserve Chair1

Americans have among the highest living standards in the world and have enjoyed rising living standards for decades. Median household income in the United States in 2015 was $56,516, up from $49,276 in 2010.2 However, gains in household income have not been evenly distributed across all income groups. Income inequality has been increasing in the United States since the 1970s, peaking in 20133 (Figure 1). A 2015 Gallup poll found that 63 percent of Americans feel that the distribution of U.S. money and wealth is unfair.4 While many factors contribute to income and wealth inequality, the role of education is a key piece of the puzzle.

Figure 1: U.S. Income Inequality a Rising Trend

NOTE: The Gini coefficient (also known as the Gini ratio or index) is a common measure of income inequality within a nation. It gauges income inequality on a scale from 0 to 1: The higher the number, the higher the level of inequality. The lowest U.S. value was 0.386 in 1968, and the highest value was 0.482 in 2013. In 2015 the, Gini coefficient was 0.479.

SOURCE: FRED®, Federal Reserve Bank of St. Louis. Accessed November 22, 2016; https://fred.stlouisfed.org/graph/?g=7yKu.

The Basics

When people earn income, they use that income to do three things: pay taxes, buy goods and services (consume), and save. Saving is not spending on current consumption or taxes and involves giving up some current consumption for future consumption. The accumulation of money set aside for future spending and consumption is known as savings. Americans don't save as much as those in other industrialized nations. The U.S. personal saving rate has dropped substantially over the past 50 years (Figure 2). As of September 2016, the U.S. personal saving rate was 5.7 percent, whereas it has historically averaged 8.4 percent (since 1959).5 By comparison, German households saved 16.7 percent, on average, in 2015.6

Figure 2: U.S. Personal Saving Rate Over 50 Years

NOTE: The horizontal line indicates the average saving rate over the period.

SOURCE: FRED®, Federal Reserve Bank of St. Louis. Accessed November 22, 2016; https://fred.stlouisfed.org/graph/?g=bQZk.

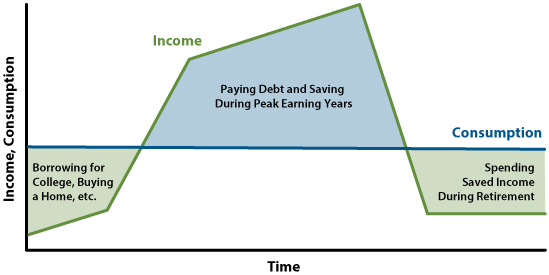

Saving is an essential component of building wealth. Wealth, also called net worth, is the total value of a person's assets, such as liquid assets (cash or something you can easily turn into cash), real estate, businesses, and cars, minus any liabilities (money owed; debt). Saving to build wealth is an important part of financial planning. And debt is not necessarily a bad thing. Because income tends to start low at younger ages, borrowing (taking on debt) allows people to have things now and pay for them over time. In economic terms, this is called smoothing consumption. Income then tends to increase in middle age and decrease when people retire. Economists often use the life cycle theory of consumption and saving to explain this phenomenon. As shown in the model (Figure 3), people tend to borrow to purchase homes, cars, or an education when they are young, pay down debt and save a portion of their income during their peak working and earning years, and finally spend their saved money during retirement. Within this pattern of planned borrowing and saving, the hump-shaped pattern of income (the curved line) allows for smooth consumption (the horizontal line) across the lifecycle. Thus, saving—to build wealth—is essential for a higher quality of life during retirement.

Figure 3: A Model of Saving and Spending: The Life Cycle Theory of Consumption and Saving

Two similar terms must be differentiated here: Income is the payment people receive for providing resources in the marketplace. For example, people often receive paychecks twice a month. You may have heard people discuss the flow of income. Saving involves setting some of the flow of income aside to increase wealth. Wealth is the accumulation—or stock—of saved money. Notice that turning the flow of income into a stock of wealth requires saving money. There are several options for saving, including saving in a savings accounts or saving through the purchase of financial assets, which is called financial investment. People invest in financial assets with the aim of "making money"—they hope to earn interest, dividends, profits, and/or capital gains in the future.

Education and Income

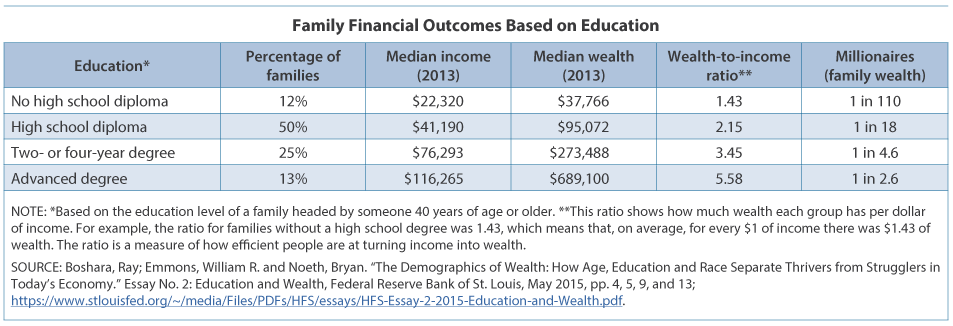

The relationship between education and income is strong. Education is often referred to as an investment in human capital. People invest in human capital for similar reasons people invest in financial assets, including to make money. In general, those with more education earn higher incomes (see the table). The higher income that results from a college degree is sometimes referred to as the "college wage premium." Research shows that this premium has grown over time.7 In addition, in general, the more skills people have, the more employable they are. As a result, workers with more education have a lower average unemployment rate than those with less education (Figure 4).

Figure 4: Unemployment Declines as Education Increases

NOTE: In November 2016, the overall U.S. unemployment rate was 4.6 percent, but level of education matters. The unemployment rate for college graduates was 2.3 percent, while that for those with less than a high school diploma was 7.9 percent.

SOURCE: FRED®, Federal Reserve Bank of St. Louis. Accessed December 21, 2016; https://fred.stlouisfed.org/graph/?g=8ds7.

Education and Wealth

The relationship between education and wealth is also strong. Of course, earning a higher income makes saving easier, and saving is necessary to build wealth. Those with lower incomes have a flatter (non-humped) income pattern, which makes saving and paying down debt more difficult. But those with more education also tend to make financial decisions that contribute to building wealth.8 It is important to realize, however, that anyone can follow the financial behaviors that well-educated families tend to practice, such as these:

- Have some liquid assets. Liquid assets can help relieve financial distress during a difficult time without having to sell assets or accumulate debt. Liquid assets include savings accounts, stocks, and bonds.

- Diversify. To diversify means to invest in various financial instruments to reduce risk. In addition to tangible assets such as houses and cars, those with higher levels of education also tend to hold a greater share of their savings in stocks, bonds, and businesses, which tend to provide higher returns (but also more risk of loss).

- Keep debt low relative to assets. Those with low debt relative to assets pay lower interest rates. Those with high debt relative to assets pay higher interest rates, which can make it difficult to save. And, over longer periods, both savings and debt are susceptible to the effects of compound interest—which means that savings (or debt) can grow at exponential rates over time.9

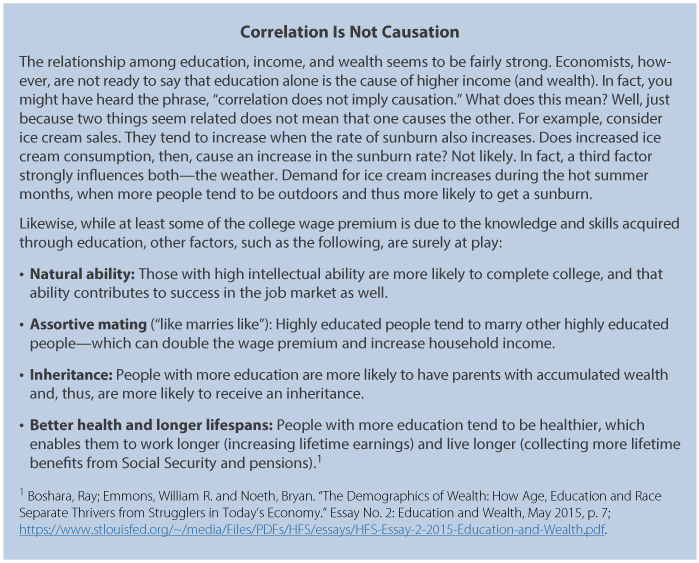

It is important to realize, however, that the relationship among education, income, and wealth is more complicated than simply more education yielding a higher income and more wealth. Factors such as natural ability and family background also impact both income and wealth and are not caused by having more education (see the boxed insert).

The Role of Financial Literacy

Research shows that up to half of wealth inequality may be caused by differences in financial literacy.10 That is, many people do not have the skills or ability to manage their money effectively. As a result, they are more likely to use costly home loan (mortgage) products,11 pay higher transaction costs and fees, and use high-cost borrowing options.12 High-cost borrowing includes the use of payday loans and businesses such as pawn shops and rent-to-own stores.13 Currently only 20 states require high school students to take a course in economics and only 17 states require a course in personal finance.14 Research has shown, however, that such education makes a difference: Students in states with financial education requirements have lower loan delinquency rates and higher credit scores relative to students in states without financial education requirements.15

Conclusion

Income and wealth inequality have been on the rise in the United States for decades. Research indicates that the level of education is strongly related to both income and wealth. Households with higher levels of education tend to have more liquid assets to withstand financial storms, diversify their savings (investments), and maintain low levels of debt relative to assets. These financial behaviors are effective strategies for building income into wealth. Because much of wealth building can be tied to financial decisionmaking, it is likely that financial literacy can play a key role in reducing wealth inequality over time.

Notes

1 Yellen, Janet L. "Perspectives on Inequality and Opportunity from the Survey of Consumer Finances." Board of Governors of the Federal Reserve System, 2014; http://www.federalreserve.gov/newsevents/speech/ye....

2 U.S. Bureau of the Census. Median Household Income in the United States [MEHOINUSA646N], retrieved from FRED, Federal Reserve Bank of St. Louis, November 22, 2016; https://fred.stlouisfed.org/graph/?g=580N.

3 Federal Reserve Bank of St. Louis. "How Has Income Changed over the Years?" On The Economy (blog); June 30, 2016; https://www.stlouisfed.org/on-the-economy/2016/june/how-has-income-inequality-changed-years.

4 Newport, Frank. "Americans Continue to Say U.S. Wealth Distribution Is Unfair." May 4, 2015; Gallup; http://www.gallup.com/poll/182987/americans-continue-say-wealth-distribution-unfair.aspx.

5 U.S. Bureau of Economic Analysis, Personal Saving Rate [PSAVERT], retrieved from FRED®, Federal Reserve Bank of St. Louis, November 22, 2016; https://fred.stlouisfed.org/graph/?g=580A.

6 Beisemann, Leonie. "A Dash of Data: Spotlight on German Households." OECD Insights, February 11, 2016; http://oecdinsights.org/2016/02/11/a-dash-of-data-spotlight-on-german-households/.

7 Valletta, Rob. "Higher Education, Wages, and Polarization." Federal Reserve Bank of San Francisco Economic Letter. January 12, 2015; http://www.frbsf.org/economic-research/publications/economic-letter/2015/january/wages-education-college-labor-earnings-income/.

8 Boshara, Ray; Emmons, William R. and Noeth, Bryan. "The Demographics of Wealth: How Age, Education and Race Separate Thrivers from Strugglers in Today's Economy." Essay No. 2: Education and Wealth, May 2015; https://www.stlouisfed.org/~/media/Files/PDFs/HFS/essays/HFS-Essay-2-2015-Education-and-Wealth.pdf.

9 Boshara, Ray; Emmons, William R. and Noeth, Bryan. "The Demographics of Wealth: How Age, Education and Race Separate Thrivers from Strugglers in Today's Economy." Essay No. 2: Education and Wealth, May 2015; https://www.stlouisfed.org/~/media/Files/PDFs/HFS/essays/HFS-Essay-2-2015-Education-and-Wealth.pdf.

10 Lusardi, Annamaria; Michaud, Pierre-Carl and Mitchell, Olivia S. "Optimal Financial Knowledge and Wealth Inequality." NBER Working Paper 18669, January 2013; http://www.nber.org/papers/w18669.pdf.

11 Moore, Danna. "Survey of Financial Literacy in Washington State: Knowledge, Behavior, Attitudes, and Experiences." Technical Report 03-39, Washington State University Social and Economic Sciences Research Center, December 2003.

12 Lusardi, Annamaria and Tufano, Peter. "Debt Literacy, Financial Experiences, and Overindebtedness." NBER Working Paper 14808, March 2009.

13 Lusardi, Annamaria and de Bassa Scheresberg, Carlo. "Financial Literacy and High-Cost Borrowing in the United States." NBER Working Paper 18969, April 2013.

14 Council for Economic Education. Survey of the United States: Economic and Personal Finance Education in Our Nation's Schools, 2016; http://councilforeconed.org/wp/wp-content/uploads/2016/02/sos-16-final.pdf.

15 Brown, Alexandra; Collins, J. Michael; Schmeiser, Maximilian and Urban, Carly. "State Mandates Financial Education and the Credit Behavior of Young Adults." Finance and Economic Discussion Series 2014-68, Federal Reserve Board, 2014; https://www.federalrese.gov/pubs/feds/2014/201468/201468pap.pdf.

© 2017, Federal Reserve Bank of St. Louis. The views expressed are those of the author(s) and do not necessarily reflect official positions of the Federal Reserve Bank of St. Louis or the Federal Reserve System.

Glossary

Asset: A resource with economic value that an individual, corporation, or country owns with the expectation that it will provide future benefits.

Capital gains: A profit from the sale of financial investments.

Compound interest: Interest computed on the sum of the original principal and accrued interest.

Credit score: A number based on information in a credit report used to indicate a person's credit risk.

Delinquency rate: The number of loans that have delinquent payments relative to the total number of loans.

Financial asset: A contract that states the conditions under which one party (a person or institution) promises to pay another party cash at some point in the future.

Financial investment: Placing money in a savings account or in any number of financial assets, such as stocks, bonds, or mutual funds, with the intention of making a financial gain.

Financial literacy: Having knowledge of financial matters and applying that knowledge to one's life.

Human capital: The knowledge and skills that people obtain through education, experience, and training.

Income: The payment people receive for providing resources in the marketplace.

Payday loan: A small, short-term loan that is intended to cover a borrower's expenses until his or her next payday. May also be called a paycheck advance or a payday advance.

Transaction costs: The costs associated with buying or selling a good, service, or financial asset.