Understanding the Speed and Size of Bank Runs in Historical Comparison

In late 2022 and early 2023, a number of banks experienced deposit runs that were extraordinarily fast and large by historical standards. To explain these historically unprecedented developments, banking regulators have focused on three factors: (i) changes in technology that have enabled faster withdrawals, (ii) social media that facilitated information dissemination and coordination among depositors, and (iii) uninsured deposits that were concentrated among bank customers with connections to each other (Federal Reserve, 2023a and 2023b; FDIC, 2023a and 2023b; New York DFS, 2023; California DFPI, 2023).

This essay provides historical comparisons to help elucidate how these factors may have increased the severity of recent runs relative to other severe runs that took place in 1984 and 2008—the most severe runs in US history since the Great Depression and until recently.

It appears that technological improvements can explain some of the increase in speed, but large increases in speed likely only apply to household and small business depositors. Major corporations, which were the predominant source of deposit withdrawals in prior run episodes at the largest banks, already had the ability to withdraw funds in an automated electronic manner since the late 1970s. Indeed, the crisis at Continental Illinois in 1984 was described as a worldwide "lightning fast electronic run" (Sprague, 1986, p. 149). By 2008 and certainly by 2023, technological advances included extension of electronic banking to smaller businesses and households and availability of online banking anywhere through smart phones rather than at dedicated computer terminals. Such advances likely sped up many deposit withdrawals by several hours or a day or two compared with phone calls, faxes, or in-person banking. But little in the historical record suggests depositors in 1984 and 2008 waited several days to make withdrawals because of technological limitations.

As a result, the rapid pace of recent runs may owe more to the other factors identified by regulators. The most significant departure from historical comparisons is that depositors at banks that experienced runs recently were unusually connected with or similar to each other. As a result, they withdrew funds in coordinated or similar ways. At Silicon Valley Bank, depositors were connected through common venture capital backers and coordinated their withdrawals through smartphone communications and social media. At Signature Bank and Silvergate Bank, large portions of depositors were crypto-asset firms that used the two banks for real-time payments with each other, business models based on moving money instantly. These crypto-asset industry depositors may also have been particularly sensitive to counterparty risk given the volatility in crypto-asset markets over the previous year.

Comparing the Size and Speed of Runs Historically

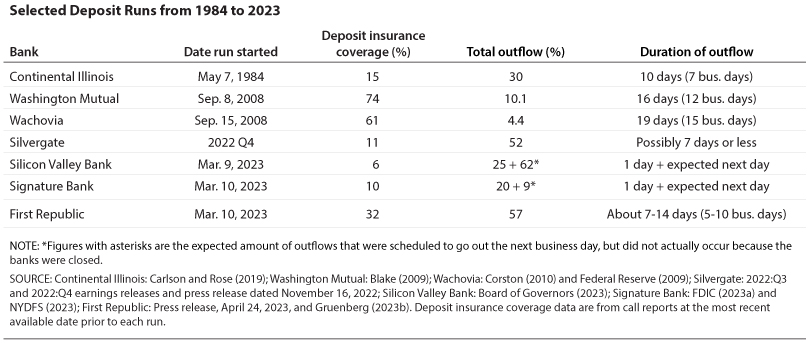

The table details the speed and size of the most severe bank runs in 1984, 2008, and 2023. Continental Illinois was around the 8th largest bank in 1984, making it the most high-profile bank to experience a crisis between the Great Depression and the 2008 financial crisis. In 2008, Wachovia, which was a distressed bank acquired by Wells Fargo, and Washington Mutual, which failed, were the 4th and 6th largest at the time. Of the banks that experienced runs since late 2002, First Republic was the 14th largest at the time, while SVB was the 16th, Signature the 29th, and Silvergate the 128th.

The most severe of the runs listed prior to 2022 is Continental's, involving the loss of 30% of its funding in 10 days. In 2008, Wachovia and Washington Mutual were the largest banks to experience what were called "massive" deposit runs at the time, involving 4.4% and 10% of deposits, respectively.1

In comparison, the most severe run recently was at Silicon Valley Bank, which lost 25% of its deposits in one day and was closed before an additional 62% was scheduled to flow out the next. At Signature, 20% of its deposits were withdrawn "in a matter of hours" (NYDFS, 2023, p. 5). At First Republic, customers withdrew about 14% of deposits on the first day, 23% the next business day, and an additional 20% over the remainder of the run (Gruenberg, 2023b, p. 10).2 Finally, I estimate Silvergate's run may have been largely completed in about 7 days, assuming that the starting point was when FTX paused withdrawals on November 8, 2022, and using information about average deposits as of a November 15 press release and quarter-end.3

Explaining the Increased Speed Compared with Historical Episodes

Electronic Withdrawal Technology

Banking regulators have noted in 2023 that "advances in digital banking" have enabled "immediate" withdrawals of funding with "unprecedented ease" (Federal Reserve, 2023a, p. 2; FDIC, 2023b, p. 27; NYDFS, 2023, p. 5).

This concern has been building for at least 39 years, since Continental's crisis in 1984. By the late 1970s, major corporations were already commonly using electronic bank account services and had the ability to execute automated withdrawals. Indeed, banks and major corporations were at the forefront of computer and communications technology. At the time, Continental offered a software package that provided customers with cash management services from their own computer terminals. Through "data grade lines supplied by Telenet, a subsidiary of General Telephone and Electronics," a Continental customer had "the ability to instruct the bank's units to effect transfers of funds to his accounts anywhere in the world" (Walker, 1980, pp. 112-39). Banks had the ability to connect to computers at the Federal Reserve Bank in their District to automatically wire funds, a process that took "only a few minutes" by 1977 (Federal Reserve Bank of St. Louis, 1978, p. 12). By 1982, in the Chicago Fed District, where Continental was located, more than 500 banks and thrifts "enjoyed direct on-line service" (Federal Reserve Bank of Chicago, 1982, p. 16).

In adopting electronic banking technology, Continental may have been an early leader in some respects. Its international data linkages were particularly advanced because of its desire to coordinate with its overseas office in Brussels (Branscomb, 1983, p. 1005). But Continental was not alone. Stevens (1984) describes large corporations as having widely integrated computerized telecommunications for bank wire transfers into their real-time accounting systems. Likewise, Ahwesh (1990) describes corporate customers as having dial-in automated access to their banks' wire rooms and that 70% or more of banks' wire activity at that time was the result of these automated electronic access methods.

As a result, the Continental Illinois crisis in 1984 was already a "lighting fast removal of large deposits from around the world by electronic transfer," as described by Irvine Sprague, an FDIC official at the time (p. 149). Sprague noted that while the bank's lobby was calm, the wire room is where the bank became aware of the withdrawal requests: "Here, the employees knew what was happening as withdrawal order after order moved on the wire, bleeding Continental to death. Some cried" (p. 153). The electronic nature of the run on Continental attracted widespread press commentary, given the relative novelty of the technology. One reporter noted that "Today through an electronic button you can empty out deposits overnight. It's different."4 Another observed "In the late 20th century, runs are caused more often by an electronic phenomenon, the ability to withdraw money electronically."5 During congressional hearings about Continental's crisis, Representative Chalmers Wylie noted that "electronic communications make it possible for institutions to raise or lose funds practically instantaneously" (US Congress, 1984, p. 77).

Continental's computer-age run was a preview of the future. In 1988, a Texas bank also known as First Republic failed in what the FDIC called an "electronic run, via ATMs and wire transfers" (FDIC, 1998, p. 598). By the time Wachovia and Washington Mutual experienced their deposit runs in 2008, these electronic systems had been in place for decades: At Washington Mutual, Grind (2012, p. 212) describes how customers "didn't line up by the hundreds at branches" but instead transferred money online or visited ATMs. Wachovia's run was similarly described as a "silent" one.6

Certainly, electronic banking has improved since 1984. By 2008, online banking was accessible to household depositors and small businesses. By 2022, withdrawals could be made from smartphones anywhere, not just at dedicated computer terminals at major corporate headquarters. Depositors may also have been more comfortable by 2023 using online options. Yet, there is little indication that depositors waited several days in 1984 or 2008 to make withdrawals because of technological limitations. Although withdrawing money by check is not the preferred method for a large depositor with hundreds of millions of dollars, by the 1970s check processing times averaged a little under 2 days (Quinn and Roberds, 2008, p. 20). Indeed, even the bank runs of the Great Depression were not necessarily mainly the result of in-person withdrawals. Rather, "most money left banks as wire transfers" (Fuller, 2014, p. 158) using the Federal Reserve's Fedwire network. Krost (1938) emphasizes the importance of large depositors in the 1930s who moved money between banks in "invisible runs" and not by visiting a bank in person. Banks also take withdrawal orders by phone and fax.

Overall, technological changes since the 1970s appear capable of speeding up withdrawals for smaller uninsured depositors by a matter of hours or a day or two. But it is difficult to view depositors in 1984 or 2008 as delayed by several days by the technology of the time. Moreover, as reviewed in the next section, major corporations have accounted for the large bulk of funds withdrawn during runs.

Large Corporate Depositors

Available evidence indicates that major corporations, with hundreds of millions of dollars in deposits, were the main holders of large uninsured accounts and were the major drivers of runs in 1984, 2008, and 2022-2023. In comparison, household and small business depositors appear to have played a limited role.

- Continental Illinois raised large amounts of funding from other banks, money market funds, and nonfinancial corporations. Its top 10 creditors provided the bank with 9% of its funds, for an average of almost $300 million each, and withdrew 2% of the bank's liabilities themselves (Carlson and Rose, 2019).

- At Wachovia, about half of its uninsured deposits were "comprised of corporate, non-time deposits that are considered highly sensitive" (FDIC, 2008). A run occurred when "corporate customers began to pull uninsured deposits."7

- At Washington Mutual, few details about corporate depositors are available, but the concentration of deposit outflows again points to corporate depositors. "Most of the runoff ($6.6B) came from uninsured accounts and approximately a third of that was from accounts over $500.0 million" (US Permanent Committee, 2011, p. 1094).

Likewise, the 2023 bank runs appear to have been largely the result of large corporate depositors with hundreds of millions of dollars that accounted for the bulk of uninsured deposits:

- Silvergate's run was concentrated among the bank's crypto-asset clients, which supplied almost 90% of the bank's deposits and withdrew 68% of their funds. Silvergate's largest 10 depositors accounted for 48% of its deposits, for an average of $630 million each, and the average crypto-asset customer held about $7 million.8

- Signature reportedly had pursued a growth strategy "based on the generation of large commercial deposits" from private equity and crypto-asset clients (FDIC, 2023a, p. 10). Crypto-asset firms in particular represented 30% of its deposits at peak (NYDFS, 2023, p. 10). The largest 60 depositors accounted for 40% of its deposits, for an average of $592 million each and the 4 largest accounted for about 15% of deposits, for an average of $2.4 billion each (FDIC, 2023a, p. 11). The run was the result of only 1,600 withdrawals that averaged $11.6 million (NYDFS, 2023, p. 32).

- At Silicon Valley, the largest 10 depositors accounted for 8% of its deposits, for an average of $1.3 billion each (Gruenberg, 2023a). Both its rapid deposit growth from 2019 to 2021 and its outflows in 2023 were attributed to venture-capital-backed technology and life sciences firms and private equity clients (Federal Reserve, 2023a, pp. 18, 53).

- First Republic's depositor base has so far not been described in much detail. Its deposits were 63% from businesses and were more concentrated than average since the bank noted that it had one-fifth the amount of depositors compared with other banks with similar asset sizes.9

Distinct Depositor Bases

The depositors at Silvergate, Signature, and SVB were heavily concentrated in specific industries and connected to each other. As a result, these depositors were much more likely to behave in coordinated or similar ways. While Continental also had very low insurance coverage and relied on large corporations to a substantial degree, those corporations were from various corners of the financial and nonfinancial economy, not concentrated in any one sector. Washington Mutual and Wachovia had significantly more-diversified depositor bases, including more-substantial insured retail deposits.

Crypto-asset firms were reportedly attracted to Silvergate and Signature in large part because of the payment networks they operated, known as the Silvergate Exchange Network (SEN) and Signet, respectively. These crypto-asset clients used these networks to transfer funds to each other in real time, avoiding interbank delays. As a result, these depositors were unusually skilled at and accustomed to moving funds very quickly. These depositors had also experienced large volatility in crypto-asset markets during 2022, including the failure of FTX in November 2022, which may have caused them to be particularly sensitive to signs of financial problems and fast to react. A Silvergate official said "we had clients that were proprietary traders, market makers that had been doing business with each other for sometimes 6, 8 years, that just stop[ped] doing business with each other and pulled their—essentially pulled all their deposits.10 This quote indicates that depositors at Silvergate likely had some awareness of each others' actions since they could observe whether other counterparties continued to do business on Silvergate's payment network.

Depositors at Silicon Valley Bank reportedly received advice from their venture capital backers to withdraw funds and communicated with each other during the run, drawing on their pre-existing connections to each other. In addition, Silicon Valley Bank also had some deposits from crypto-asset firms, including $3.3 billion from the stablecoin issuer Circle, alone accounting for 2% of deposits.

Less information is available about First Republic's depositors. Gruenberg (2023b) notes the bank had customers employed in and related to the venture capital and tech industries, but they do not appear to have had common venture capital backers in the same was as Silicon Valley Bank. More information about First Republic's run, if it becomes available through reports by federal regulators, may provide valuable additional perspective.

Conclusion

Policymakers have examined recent bank failures closely and are taking seriously the question of why deposit runs were so fast and large by historical standards. They have pointed to technology, social media, and the nature of the depositor base at each bank as factors that increased the speed of runs. From an historical perspective, the most unusual characteristic of the bank runs in 2022-2023 is the depositor base at failed institutions. While advances in technology likely also contributed to increased speeds, the run on Continental Illinois in 1984 was already a highly electronic one. This analysis is likely most applicable to the supervision of very large banks with significant and concentrated corporate deposits. At such banks, if connections and similarities among depositors are especially important in driving the speed of runs, then so is supervision and regulation that gathers information about the likelihood of depositors behaving in similar ways during a crisis. Such information could help tailor stress testing assumptions or price deposit insurance risk. On the other hand, if changes in technology are more important, then deposit outflow assumptions may need to be raised for all types of uninsured depositors across the board.

Notes

1 At Citibank—not listed in Table 1 since the details of its "global run on deposits" have never been publicly disclosed—supervisors feared a run rate of 2% per day and noted that a 7.2% run would exhaust available cash (SIGTARP, 2011). Several additional smaller banks experienced runs in 2008, including National City, Sovereign, and IndyMac as described by Rose (2015).

2 Gruenberg (2023b) states that the outflow on the first day was 17% of deposits, but for consistency with other estimates I report it as 14%, calculated using a denominator either from December 31, 2022, or March 9, 2023. In addition, while First Republic's press release described the run as stabilizing "beginning the week of March 27, 2023," Gruenberg (2023b) states withdrawals "stabilized during the week ending March 24." The table reports the shorter window described by Gruenberg.

3 Silvergate reported average deposits from digital assets (DA) customers of $9.8 billion from October 1 to November 15 and $7.3 billion for the quarter as a whole. From these numbers it is possible to back out the average value after November 15 and compare it with quarter-end. However, one adjustment is necessary, as the $9.8 billion figure excluded FTX. Silvergate separately announced that FTX had accounted for "less than 10%" of its deposits on September 30, 2022. If we assume that "less than 10%" means 9%, then FTX deposits were about $1.1 billion, implying that average DA deposits up to November 15 were $10.9 billion. These figures imply average DA deposits after November 15 were around $3.7 billion, approximately the same as the quarter-end figure of $3.8 billion, implying the run had been completed by November 15.

4 Wall Street Journal. "Confidence game." May 25, 1984, p. 1.

5 Gruber, W. "Banking: Banker calls deficit 'dangerous force'." Chicago Tribune, May 31, 1984.

6 Rothacker, Rick. "$5 billion withdrawn in one day in silent run." Charlotte Observer, October 11, 2008.

7 American Banker. "Wachovia's End." October 13, 2009. Available online

8 See Silvergate's earnings reports for 2022:Q3 and 2022:Q4 and its 2022:Q3 SEC filing.

9 First Republic 2022:Q4 earnings release, pp. 16-17.

10 Silvergate investor call, January 5, 2023.

References

Ahwesh, Philip C. "Addressing Risk in the Large-Dollar Payments System." The Bankers Magazine. July/August 1990, pp. 12-18.

Blake, Thomas. Declaration to the United States Bankruptcy Court, District of Delaware, Chapter 11 Case No. 08-12229 (MFW), Bankruptcy of Washington Mutual, 2008.

Board of Governors of the Federal Reserve System. "Review of the Federal Reserve's Supervision and Regulation of Silicon Valley Bank," 2023a; available online.

Board of Governors of the Federal Reserve System. "Financial Stability Report," May 2023b; available online.

Branscomb, Anne W. "Global Governance of Global Networks: A Survey of Transborder Data Flow in Transition." Vanderbilt Law Review, vol. 36, no. 4, May 1983; available online.

California Department of Financial Protection and Innovation. "Review of DFPI's Oversight and Regulation of Silicon Valley Bank," 2023; available online.

Carlson, Mark and Jonathan Rose. "The incentives of large sophisticated creditors to run on a too big to fail financial institution." Journal of Financial Stability, 2019; available online.

Corston, John. "Systemically Important Institutions and the issue of Too Big to Fail." Testimony before the Financial Crisis Inquiry Commission, 2010; available online.

Federal Deposit Insurance Corporation. Managing the Crisis, 1998; available online.

Federal Deposit Insurance Corporation. "Memo to the FDIC Board of Directors, Re: Wachovia," Financial Crisis Inquiry Commission document 140, 2008; available online.

Federal Deposit Insurance Corporation. "FDIC's Supervision of Signature Bank." April 28, 2023a; available online.

Federal Deposit Insurance Corporation. "Options for Deposit Insurance Reform," 2023b; available online.

Federal Reserve Bank of Chicago. Annual Report, 1982; available online.

Federal Reserve Bank of St. Louis. "Operations of the Federal Reserve Bank of St. Louis – 1976." Review, vol. 59, no. 2, 1978; available online.

Federal Reserve Board. "Wachovia Case Study," Financial Crisis Inquiry Commission document 994, 2009; available online.

Fuller, Robert Lynn. Phantom of Fear. McFarland, 2014.

Grind, Kirsten. The Lost Bank. Simon & Schuster, 2012.

Gruenberg, Martin. Remarks on Recent Bank Failures and the Federal Regulatory Response before the Committee on Banking, Housing, and Urban Affairs, United States Senate, March 28, 2023a; available online.

Gruenberg, Martin. Remarks, "Oversight of Financial Regulators: Financial Stability, Supervision, and Consumer Protection in the Wake of Recent Bank Failures" before the Committee on Banking, Housing, and Urban Affairs, United States Senate, May 18, 2023b; available online.

Krost, Martin. "A Sample Study of the Records of Suspended Banks." Federal Reserve Board study, 1938; available online.

New York State Department of Financial Services. (2023) "Internal Review of the Supervision and Closure of Signature Bank," 2023; available online.

Rose, Jonathan D. "Old-Fashioned Deposit Runs," Finance and Economics Discussion Series 2015-111. Washington: Board of Governors of the Federal Reserve System, 2015; available online.

Special Inspector General for the Troubled Asset Relief Program (2011). "Extraordinary Financial Assistance Provided to Citigroup, Inc," 2011; available online.

Sprague, Irvine H. Bailout: An Insider's Account of Bank Failures and Rescues. New York: Basic Books, 1986.

Stevens, E. J. (1984). "Risk in Large-Dollar Transfer Systems." Economic Review, Fall 1984, Federal Reserve Bank of Cleveland, 1984; available online.

United States Senate Permanent Committee on Investigations. (2011) Wall Street and the financial Crisis: Anatomy of a Financial Collapse. Report and appendix before the Permanent Subcommittee on Investigation of the Committee on Homeland Security and Governmental Affairs, United States Senate, 2011; available online.

United States Congress. "Inquiry into Continental Illinois Corp. and Continental Illinois National Bank." Hearings Before the Subcommittee on Financial Institutions Supervision, Regulation and Insurance, 98th Congress, 1984; available online.

Walker, Robert. Testimony, Hearings on "International Data Flow," before a subcommittee of the Committee on Government Operations, House of Representatives, Ninety-sixth Congress, second session, p. 112, 1980; available online.

© 2023, Federal Reserve Bank of St. Louis. The views expressed are those of the author(s) and do not necessarily reflect official positions of the Federal Reserve Bank of St. Louis or the Federal Reserve System.