Inflation, Part 2: How Do We Construct and Choose an Index?

Understanding inflation can be challenging. Consumers may not know how rising prices correspond to the multiple estimates published by government bureaus or why the data vary. According to the Bureau of Labor Statistics' (BLS's) consumer price index (CPI), prices increased 8.3% last April from the year before; according to the Bureau of Economic Analysis's (BEA's) personal consumption expenditures (PCE) price index, they increased 6.3%. What are consumers to make of these indexes—and why do they differ?

Constructing an Index

As we discussed in Part 1 of this series, the CPI and PCE price indexes attempt to measure the average price level of consumer goods and services. They go about it in different ways, however, hence the discrepancy in the numbers.

When economists construct a price index, they must decide what items—and how many of each item—to include in the index's "basket." The CPI and PCE differ in large part because their baskets are constructed differently, with different "scopes" in mind. For one thing, the CPI focuses on urban consumers—people living in cities—whereas the PCE focuses on all consumers in the country.

More fundamentally, the CPI is designed to reflect out-of-pocket purchases made directly by consumers; the PCE instead reflects purchases made both by and on behalf of consumers, regardless of who or what entity directly pays. Consequently, expenditures made for consumers by employers, nonprofits, governments, and other institutions (such as health care services paid for by employers for employees) are included in the PCE but not the CPI.

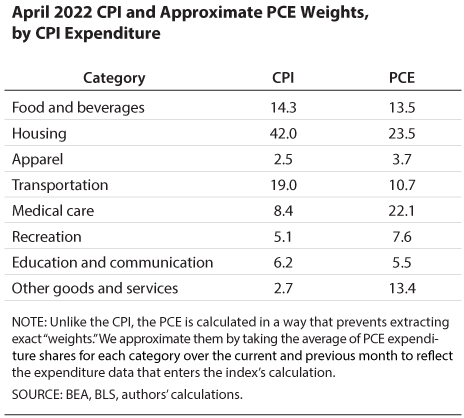

The indexes also differ in how much of each item they include (or, equivalently, how much they "weight" each item) in their baskets. Both indexes reflect the amounts of each item purchased by (or on behalf of) the typical consumer—but they rely on different data sources to estimate these purchases. Moreover, CPI weights come from household surveys, whereas PCE weights come from business surveys.

Constructing any price index involves other, less obvious, decisions. For instance, the CPI and PCE both adjust prices to account for changing quality (a decision the BLS1 and BEA2 have defended against frequent misconceptions). They both seasonally adjust price changes, though in slightly different ways. They also change the composition of their baskets, though at different frequencies: The CPI basket is updated every two years, while the PCE basket is updated every month.

Consequently, the two baskets can differ substantially, as the table shows. For instance, housing is a much larger portion of the CPI basket than of the PCE basket, while the opposite is true for medical care. These differences can have substantial effects on inflation estimates: If one category has higher inflation and that category makes up a bigger portion of one of the indexes, that index will (all else equal) grow faster as well.

Choosing an Index

The CPI is arguably more popular than the PCE. It is used to calculate cost-of-living adjustments for Social Security and other government programs; Treasury inflation-protected securities are based on it, and not the PCE; and it is released earlier than the PCE, lending itself to more press coverage.

The Federal Reserve, however, targets the PCE—believing it to be a better measure of true inflation. In one report to Congress,3 the Fed argued that the PCE better captures changing consumer consumption because its weight scheme is updated monthly, keeping it from being biased upward; covers a wider variety of expenditures, which is important when considering the Fed's mandate to maintain overall price stability; and can be revised by the BEA, allowing measurement and data advancements to improve and standardize the index over time

Concern that the CPI's rigid basket could bias it upward is long-standing; in 1996, the Boskin Commission estimated that the CPI overstated true cost-of-living increases by about 1.1%. As prices rise more quickly for some items than for others, consumers tend to buy less of those items and more of the cheaper alternatives (the so-called "substitution effect"). The CPI, economists argue, does not capture this as well or quickly as the PCE does.

This difference is one major reason the CPI has trended higher than the PCE over time, as the figures shows. The "chained CPI"—an alternative measure constructed by the BLS that accounts for substitution, making it more akin to the PCE—has trended much more closely to the PCE.

Concluding Thoughts

Of course, economists understand that no price index is perfect. Nonetheless, the CPI and PCE are some of the best measurements of "actual" consumer prices, and their changes are good indicators of true price inflation. Indeed, despite the indexes' many methodological differences, their measures of inflation tend to be quite similar and move at the same time, in the same ways: Their correlation since 2000 is nearly 0.99! In Part 3, we will review how the Fed views its mandate of "stable prices" according to these indexes, and how well it has historically done achieving that mandate.

Notes

1 Greenlees, John S. and McClelland, Robert B. "Addressing Misconceptions about the Consumption Price Index." Bureau of Labor Statistics Monthly Labor Review, August 2005, pp. 3-19; https://www.bls.gov/opub/mlr/2008/08/art1full.pdf.

2 Wasshausen, Dave and Moulton, Brent R. "The Role of Hedonic Methods in Measuring Real GDP in the United States." 31st CEIS Seminar—Are We Measuring Productivity Correctly, 2007 edition, pp. 97-112; https://www.bea.gov/sites/default/files/papers/P2006-6_0.pdf.

3 Board of Governors of the Federal Reserve System. "Monetary Policy Report to the Congress Pursuant to the Full Employment and Balanced Growth Act of 1978." February 2000; https://www.federalreserve.gov/boarddocs/hh/2000/february/fullreport.pdf.

© 2022, Federal Reserve Bank of St. Louis. The views expressed are those of the author(s) and do not necessarily reflect official positions of the Federal Reserve Bank of St. Louis or the Federal Reserve System.