Get an Education, Even if It Means Borrowing

"I would get my student loans, get money, register and never really go. It was a system I thought would somehow pan out."

—Ray Romano

"So, what are your plans after graduation?" The further along you get in high school, the more you're going to hear this question. There are a lot of alternatives. You may be planning to attend a career school for cosmetology or construction, for example. Another option might be to obtain a two-year certificate from a community college. Careers as a truck driver, phlebotomist, certified nursing assistant, or heating and air conditioning technician are available with a two-year certificate. Or you may be planning to attend a four-year institution. All of these educational options have at least one thing in common—they come with a price.

The Price of Education

The price of obtaining an education beyond high school varies greatly, and it depends on many factors, such as the type and level of training you desire, the location of the school, the type of school, and the grants and scholarships you are able to obtain.

Some career paths are obviously more expensive than others. For example, to become a dentist, you must obtain a four-year bachelor's degree followed by a four-year dental program degree. However, you can teach in a dental hygienist program with a master's degree, and you can become a dental hygienist with an associate's degree.1

Location also matters. If you attend a school within driving distance, you can live at home and save the cost of room and board. If you attend a school far from home, you have the additional expense of housing and airfare; and if you attend school in a high-cost area, such as either the west or east coast, living expenses will be greater.

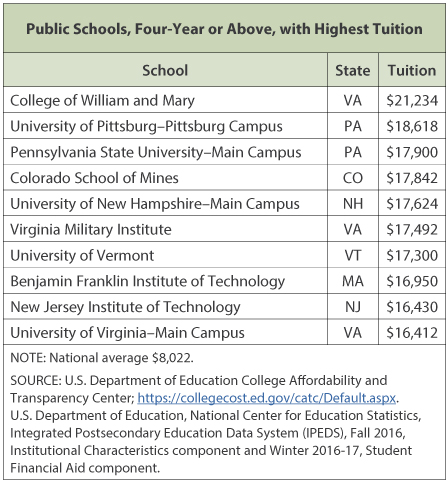

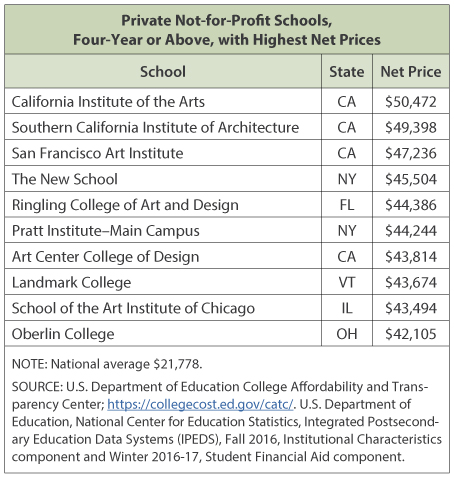

Public and private schools can present different prices, but don't eliminate private schools from your list until you investigate. There can be, and most often is, a significant difference between the published price of tuition and fees and the price after grants and scholarships have been applied. A measure used to determine the price of attending is "net price," which is the average price students pay, including tuition and required fees, books and supplies, and room and board, after accounting for grant and scholarship money received.2 The national average net price for a public school is $12,272, while the national average net price for a private school is $21,778, so it may seem that a public school would be cheaper to attend than a private school. However, as an example, the average net price of attending Haverford College,3 a private school near Philadelphia, was $23,582 in 2016-17, while the average net price of attending Pennsylvania State University, a public school, was $25,055 (see "Postsecondary Schools: Tuition and Net Prices").4

Postsecondary Schools: Tuition and Net Prices

For grants and scholarships, fill out the Free Application for Federal Student Aid (FAFSA®—more on this later). The sooner you submit, the better your chances of receiving an award. Deadlines vary among states, so check the Federal Student Aid website.5 Even the smallest grants and scholarships can add up and significantly reduce the price you will pay. Explore local civic groups for scholarships. The awards may be as little as $200, but $200 will buy a book or pay your parking fee for a semester. Check with family employers to see if there are scholarships available for family members. Check your school of choice for incoming freshmen scholarships; and when you've chosen a major, check for department scholarships.

Student Loan: Good Investment or Needless Cost?

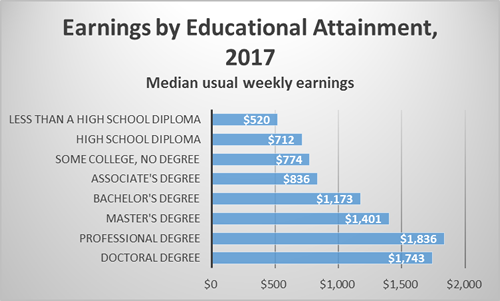

If your grants and scholarships don't quite cover all of your expenses, you might consider loans. Loans can be a valuable investment in your future because obtaining education beyond high school generally increases your lifetime earnings and provides you with a greater guarantee of employment. "A Look at Earnings and Unemployment Rates" provides an illustration of the benefits of education. Note that the median weekly wage for a person with only a high school diploma is $712, while the median weekly wage for a person with an associate's degree is $836. Multiplying the high school graduate's weekly wage by 48 years amounts to lifetime earnings of $1,777,152. Although that is a lot of money, it is significantly less than the lifetime earnings of the person with an associate's degree, which, after 46 years, would be just short of $2 million at $1,999,712. Moving up the educational attainment ladder, the next step, a bachelor's degree, would provide lifetime earnings of $2,683,824 after 44 years of working. That's nearly $1 million more than what the high school graduate might earn, and it is more than half a million more than what the person with an associate's degree might earn. In addition, note the difference in unemployment rates for college graduates and high school graduates, with no additional training. The college graduate is consistently less likely to become unemployed.

A Look at Earnings and Unemployment Rates

NOTE: Data are for persons age 25 and over. Earnings are for full-time wage and salary workers.

SOURCE: U.S. Bureau of Labor Statistics, current population survey.

SOURCE: U.S. Bureau of Labor Statistics, retrieved from FRED®, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/graph/?g=l4kP, accessed September 4, 2018.

Yes, a student loan can be the best investment you will ever make; however, proceed with caution. Never borrow more than you need to attend school. The new apartment may be much more attractive than the shabby dorm room, but if you are borrowing to have the nicer apartment, keep in mind that you may still be paying for that apartment 10 years after you move out of it. In addition, find the most cost-effective way to get the education for the career you want. For example, in-state tuition is generally much less expensive than attending a public school out of state. If you can obtain the degree you want from an in-state school, consider that option carefully. Your in-state school might not have the best football team, but unless you're playing, that's really a small consideration. Your in-state school might not have a beach or mountains, but you can visit those places on vacation with all the money you will save by not taking a loan to attend the out-of-state school.

Most importantly, finish school! Finishing school is one of the most reliable predictors of loan repayment. Sixty-eight percent of borrowers who obtained a degree had begun repayment on their loans after five years. However, among borrowers who did not complete their program of study, only 43 percent had begun repayment. One reason for this difference is that, generally, college graduates earn more money, as noted above, so they can more easily afford to make student loan payments.6

How To Obtain a Loan

The first step to college funding is the FAFSA. Just as the FAFSA is used to determine which grants and scholarships you receive, it is also used to determine your expected family contribution (EFC). Financial-aid staff at the school determines your cost of attendance (COA). The difference between your EFC and COA is your financial need, and it determines what type of loan you can receive. The FAFSA is completed online at https://fafsa.ed.gov, or you can download "myStudentAid" from the app store. The FAFSA on the Web Worksheet7 is also helpful in organizing your information.

Types of Loans

You can obtain loans privately, say, through a local bank, or you can obtain a federal student loan through the U.S. Department of Education. Private loans will vary by institution, so let's concentrate on federal direct loans.

Direct subsidized loans are available to undergraduate students with financial need. The school you are attending will determine how much you can borrow. The U.S. Department of Education will pay the interest on your loan as long as you're in school at least half-time or within the grace period (the first six months after leaving school). Notice that it's the first six months after leaving school. You might leave school because you graduated, or you might leave school because you dropped out. Either way, you are expected to begin loan payments after six months.8

Direct unsubsidized loans are available to any student attending school beyond high school. You do not have to demonstrate financial need. Your school will decide the amount you can borrow based on your cost of attending and your other sources of financial aid. Interest begins to accumulate from the day the loan is issued. A student can opt to not pay the interest while in school or during the grace period, but the interest will compound during that period and make the loan much more expensive.9

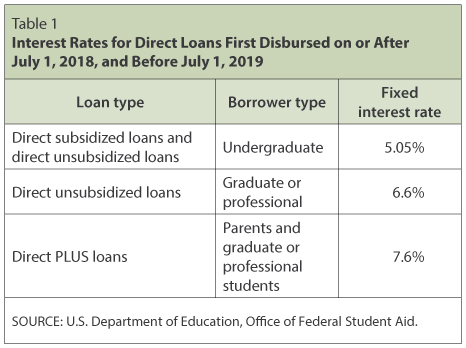

Direct PLUS loans are available to graduate or professional students who are enrolled at least half-time and working toward a graduate or professional degree. This type of loan is also available to parents of a dependent undergraduate student enrolled at least half-time.10 Table 1 shows the current interest rate on direct subsidized and unsubsidized loans, direct unsubsidized loans for students in graduate or professional programs, and direct PLUS loans.11

Payback Rules and Strategies

The standard repayment plan is a fixed monthly payment for 10 years. Basing payments on a loan amount of $5,000 at an interest rate of 5.05 percent for 10 years, the monthly payment would be $53. Imagine that you took out a loan of $5,000 for each of the four years you attended school. In this case, you would make four monthly payments of $53. (This is a simple example and does not include the accumulating interest while attending school.) So, the total monthly payment would be $212. Multiple loans may be a challenge, so you may want to combine all of your loans into a direct consolidation loan. The benefit of this loan is that you can extend the payback time to decrease the monthly payment. For example, in this case, the repayment period can be 20 years. Table 2 shows the repayment period based on amount owed.12

You're probably thinking, "Won't the additional interest over 20 years make this loan more expensive in the long run?" Well, you're right. While the monthly payment would be a much more manageable $133, the cost of the loan would be $31,920. That's $6,480 more than the same loan paid over 10 years.

Other repayment options take your income into consideration. These plans cap your monthly payment at a percentage of your discretionary income—generally between 10 and 20 percent. The loans have a duration of 20 or 25 years, and after the repayment period any remaining balance is forgiven. The monthly payment may decrease if your discretionary income decreases, but it will increase as your discretionary income increases.13

Under certain conditions, it is possible to temporarily suspend payments (although you might still have to pay interest) or to temporarily reduce your payments. If you have a direct loan, you may be eligible for the Public Service Loan Forgiveness Program. To qualify, you must work full-time for a government organization (federal, state, local, or tribal) or a not-for-profit organization or serve as an AmeriCorps or a Peace Corp volunteer.14 (Other employment may also qualify.) Under this repayment program, the remaining balance on your direct loan after 120 months (10 years) may be forgiven. Student loans cannot be eliminated through bankruptcy.

Planning Ahead

One way to avoid high student loan debt after graduation is to plan your budget before you enter college or career school. Your expenses will change from time to time, but a plan will help you keep expenses manageable. To begin with, recognize that the purpose of postsecondary education is to prepare you for the workforce. It's just that simple. All of the other attractions are nice—that is, the great location, the beautiful campus, the Greek life, the athletics, the parties. You have to decide what those amenities are worth, particularly if you are borrowing to get them.

Investigate nearby schools. Living at home and attending two years of community college, perhaps followed by two years at your local public university, could save you thousands of dollars. Submit your FAFSA as early as possible for the best grant and loan opportunities. Check with your local civic organizations, your family's employers, and your local community colleges and universities for grants and scholarships.

Conclusion

Postsecondary education is expensive, but it is probably the best investment you will ever make. Generally speaking, the higher your educational attainment, the higher your wage and the lower your chance of being unemployed. Even if you plan carefully, choose a less-expensive school, and apply for grants and scholarships, you may still need to borrow. When applying for a student loan, borrow the very minimum to get by. And, most importantly, graduate!

Notes

1 Doctorly.org. "Dentistry Educational Track"; http://doctorly.org/educational-track-for-dentists/.

2 Note: Average net price is generated by subtracting the average amount of federal government, state/local government, or institutional grant or scholarship aid from the total cost of attendance. Total cost of attendance is the sum of published tuition and required fees (lower if in-district or in-state, where applicable), books and supplies, and the weighted average for room and board and other expenses.

3 National Center for Education Statistics, College Navigator. "Haverford College: 2016-17"; https://nces.ed.gov/collegenavigator/?q=haverford+college&s=PA&ct=2&ic=1&id=212911.

4 National Center for Education Statistics, College Navigator. "Pennsylvania State University-Main Campus: 2016-17"; https://nces.ed.gov/collegenavigator/?q=pennsylvania+state+university&s=PA&ct=1&ic=1&id=214777#netprc.

5 U.S. Department of Education, Office of Federal Student Aid, Free Application for Federal Student Aid (FAFSA). "Student Aid Deadlines"; https://fafsa.ed.gov/deadlines.htm#.

6 Cooper, P. "Why Do College Dropouts Fail To Repay Their Student Loans?" Forbes. August 9, 2018; https://www.forbes.com/sites/prestoncooper2/2018/08/09/why-do-college-dropouts-fail-to-repay-their-student-loans/#6472f1bf4443.

7 U.S. Department of Education, Office of Federal Student Aid. "FAFSA on the Web Worksheet"; https://fafsa.ed.gov/.

8 U.S. Department of Education, Office of Federal Student Aid. "The U.S. Department of Education Offers Low-Interest Loans to Eligible Students to Help Cover the Cost of College or Career School"; https://studentaid.ed.gov/sa/node/49.

9 See footnote 8.

10 U.S. Department of Education, Office of Federal Student Aid. "PLUS Loans are Federal Loans that Graduate or Professional Students and Parents of Dependent Undergraduate Students can Use to Help Pay for College or Career School"; https://studentaid.ed.gov/sa/node/50.

11 U.S. Department of Education, Office of Federal Student Aid. "Understand How Interest Is Calculated and What Fees Are Associated with Your Federal Student Loan"; https://studentaid.ed.gov/sa/types/loans/interest-rates.

12 U.S. Department of Education, Office of Federal Student Aid. "The Standard Repayment Plan Is the Basic Repayment Plan for Loans from the William D. Ford Federal Direct Loan (Direct Loan) Program and Federal Family Education Loan (FFEL) Program"; https://studentaid.ed.gov/sa/repay-loans/understand/plans/standard#eligible-loans.

13 U.S. Department of Education, Office of Federal Student Aid. "If Your Federal Student Loan Payments Are High Compared to Your Income, You May Want to Repay Your Loans Under an Income-Driven Repayment Plan"; https://studentaid.ed.gov/sa/repay-loans/understand/plans/income-driven.

14 U.S. Department of Education, Office of Federal Student Aid. "What Is Qualifying Employment?"; https://studentaid.ed.gov/sa/node/91#qualifying-employment.

© 2018, Federal Reserve Bank of St. Louis. The views expressed are those of the author(s) and do not necessarily reflect official positions of the Federal Reserve Bank of St. Louis or the Federal Reserve System.

Glossary

Cost of attendance (COA): The total amount it will cost you to go to school—usually stated as a yearly figure.

Direct consolidation loan: A federal loan made by the U.S. Department of Education that allows you to combine one or more federal student loans into one new loan.

Direct loan: A federal student loan, made through the William D. Ford Federal Direct Loan Program, for which eligible students and parents borrow directly from the U.S. Department of Education at participating schools. Direct subsidized loans, direct unsubsidized loans, direct PLUS loans, and direct consolidation loans are types of direct loans.

Discretionary income: The portion of personal income available for spending after taxes and basic essentials have been deducted.

Expected family contribution (EFC): The number that's used to determine your eligibility for federal student financial aid. This number results from the financial information you provide on your FAFSA® form, the application for federal student aid.

Free Application for Federal Student Aid (FAFSA) form: A free application you can complete to apply for federal student aid.

Median: The value in an ordered set of values below and above which there is an equal number of values; the number that divides numerically ordered data into two equal halves; the middle number of a set of numbers.