Why Are Some Countries Rich and Others Poor?

"Open markets offer the only realistic hope of pulling billions of people in developing countries out of abject poverty, while sustaining prosperity in the industrialized world."1

—Kofi Annan, former United Nations Secretary-General

Many people mark the birth of economics as the publication of Adam Smith's The Wealth of Nations in 1776. Actually, this classic's full title is An Inquiry into the Nature and Causes of the Wealth of Nations, and Smith does indeed attempt to explain why some nations achieve wealth and others fail to do so. Yet, in the 241 years since the book's publication, the gap between rich countries and poor countries has grown even larger. Economists are still refining their answer to the original question: Why are some countries rich and others poor, and what can be done about it?

"Rich" and "Poor"

In common language, the terms "rich" and "poor" are often used in a relative sense: A "poor" person has less income, wealth, goods, or services than a "rich" person. When considering nations, economists often use gross domestic product (GDP) per capita as an indicator of average economic well-being within a country. GDP is the total market value, expressed in dollars, of all final goods and services produced in an economy in a given year. In a sense, a country's GDP is like its yearly income. So, dividing a particular country's GDP by its population is an estimate of how much income, on average, the economy produces per person (per capita) per year. In other words, GDP per capita is a measure of a nation's standard of living. For example, in 2016, GDP per capita was $57,467 in the United States, $42,158 in Canada, $27,539 in South Korea, $8,123 in China, $1,513 in Ghana, and $455 in Liberia (Figure 1).2

NOTE: Liberia's GDP per capita of $455 is included but not visible due to the scale. The Republic of Korea is the official name of South Korea.

SOURCE: World Bank, retrieved from FRED®, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/graph/?g=eMGq, accessed July 26, 2017.

Because GDP per capita is simply GDP divided by the population, it is a measure of income as if it were divided equally among the population. In reality, there can be large differences in the incomes of people within a country. So, even in a country with relatively low GDP, some people will be better off than others. And, there are poor people in very wealthy countries. In 2013 (the most recent year comprehensive data on global poverty are available), 767 million people, or 10.7 percent of the world population, were estimated to be living below the international poverty line of $1.90 per person per day.3 Whether for people or nations, the key to escaping poverty lies in rising levels of income. For nations specifically, which measure wealth in terms of GDP, escaping poverty requires increasing the amount of output (per person) that their economy produces. In short, economic growth enables countries to escape poverty.

How Do Economies Grow?

Economic growth is a sustained rise over time in a nation's production of goods and services. How can a country increase its production? Well, an economy's production is a function of its inputs, or factors of production (natural resources, labor resources, and capital resources), and the productivity of those factors (specifically the productivity of labor and capital resources), which is called total factor productivity (TFP). Consider a shoe factory. Total shoe production is a function of the inputs (raw materials such as leather, labor supplied by workers, and capital resources, which are the tools and equipment in the factory), but it also depends on how skilled the workers are and how useful the equipment is. Now, imagine two factories with the same number of workers. In the first factory, workers with basic skills move goods around with push carts, assemble goods with hand tools, and work at benches. In the second factory, highly trained workers use motorized forklifts to move pallets of goods and power tools to assemble goods that move along a conveyer belt. Because the second factory has higher TFP, it will have higher output, earn greater income, and provide higher wages for its workers. Similarly, for a country, higher TFP will result in a higher rate of economic growth. A higher rate of economic growth means more goods are produced per person, which creates higher incomes and enables more people to escape poverty at a faster rate. But, how can nations increase TFP to escape poverty? While there are many factors to consider, two stand out.

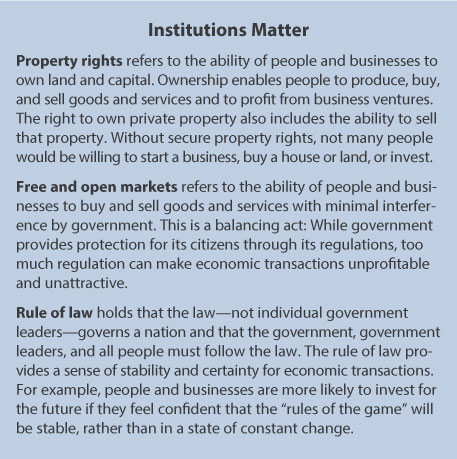

Institutions

First, institutions matter. For an economist, institutions are the "rules of the game" that create the incentives for people and businesses. For example, when people are able to earn a profit from their work or business, they have an incentive not only to produce but also to continually improve their method of production. The "rules of the game" help determine the economic incentive to produce. On the flip side, if people are not monetarily rewarded for their work or business, or if the benefits of their production are likely to be taken away or lost, the incentive to produce will diminish. For this reason, many economists suggest that institutions such as property rights, free and open markets, and the rule of law (see the boxed insert) provide the best incentives and opportunities for individuals to produce goods and services.

North and South Korea often serve as an example of the importance of institutions. In a sense they are a natural experiment. These two nations share a common history, culture, and ethnicity. In 1953 these nations were formally divided and governed by very different governments. North Korea is a dictatorial communist nation where property rights and free and open markets are largely absent and the rule of law is repressed. In South Korea, institutions provide strong incentives for innovation and productivity. The results? North Korea is among the poorest nations in the world, while South Korea is among the richest.4

NOTE: While the Republic of Korea (the official name of South Korea), China, Ghana, and Liberia had similar standards of living in 1970, they have developed differently since then.

SOURCE: World Bank, retrieved from FRED®, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/graph/?g=eMGt, accessed July 26, 2017.

While this seems like a simple relationship—if government provides strong property rights, free markets, and the rule of law, markets will thrive and the economy will grow—research suggests that the "institution story" alone does not provide a complete picture. In some cases, government support is important to the development of a nation's economy. Closer inspection shows that the economic transformation in South Korea, which started in the 1960s, was under the dictatorial rule of Park Chung-hee (who redirected the nation's economic focus on export-driven industry), not under conditions of strong property rights, free markets, and the rule of law (which came later).5 South Korea's move toward industrialization was an important first step in its economic development (see South Korea's growth in Figure 2). China is another example of an economy that has grown dramatically. In a single generation it has been transformed from a backward agrarian nation into a manufacturing powerhouse. China tried market reforms during the Qing dynasty (whose modernization reforms started in 1860 and lasted until its overthrow in 1911) and the Republic Era (1912-1949), but they were not effective. China's economic transformation began in 1978 under Deng Xiaoping, who imposed a government-led initiative to support industrialization and the development of markets, both internally and for export of Chinese goods.6 These early government-supported changes helped develop the markets necessary for the current, dramatic increase in economic growth (see Figure 2).

Trade

Second, international trade is an important part of the economic growth story for most countries. Think about two kids in the school cafeteria trading a granola bar for a chocolate chip cookie. They are willing to trade because it offers them both an opportunity to benefit. Nations trade for the same reason. When poorer nations use trade to access capital goods (such as advanced technology and equipment), they can increase their TFP, resulting in a higher rate of economic growth.7 Also, trade provides a broader market for a country to sell the goods and services it produces. Many nations, however, have trade barriers that restrict their access to trade. Recent research suggests that the removal of trade barriers could close the income gap between rich and poor countries by 50 percent.8

Conclusion

Economic growth of less-developed economies is key to closing the gap between rich and poor countries. Differences in the economic growth rate of nations often come down to differences in inputs (factors of production) and differences in TFP—the productivity of labor and capital resources. Higher productivity promotes faster economic growth, and faster growth allows a nation to escape poverty. Factors that can increase productivity (and growth) include institutions that provide incentives for innovation and production. In some cases, government can play an important part in the development of a nation's economy. Finally, increasing access to international trade can provide markets for the goods produced by less-developed countries and also increase productivity by increasing the access to capital resources.

Notes

1 Globalist. "Kofi Annan on Global Futures." February 6, 2011; https://www.theglobalist.com/kofi-annan-on-global-futures/.

2 Data from the World Bank retrieved from FRED®; https://fred.stlouisfed.org/graph/?g=erxy, accessed July 26, 2017.

3 World Bank. "Poverty and Shared Prosperity 2016: Taking on Equality." 2016, p. 4; http://www.worldbank.org/en/publication/poverty-and-shared-prosperity.

4 Olson, Mancur. "Big Bills Left on the Sidewalk: Why Some Nations are Rich, and Others Poor." Journal of Economic Perspectives, Spring 1996, 10(2), pp. 3-24.

5 Wen, Yi and Wolla, Scott. "China's Rapid Economic Rise: A New Application of an Old Recipe. Social Education." Social Education, March/April 2017, 81(2), pp. 93-97.

6 Wen, Yi and Fortier, George E. "The Visible Hand: The Role of Government in China's Long-Awaited Industrial Revolution." Federal Reserve Bank of St. Louis Review, Third Quarter 2016, 98(3), pp. 189-226; https://dx.doi.org/10.20955/r.2016.189-226.

7 Santacreu, Ana Maria. "Convergence in Productivity, R&D Intensity, and Technology Adoption." Federal Reserve Bank of St. Louis Economic Synopses, No. 11, 2017; https://doi.org/10.20955/es.2017.11.

8 Mutreja, Piyusha; Ravikumar, B. and Sposi, Michael J. "Capital Goods Trade and Economic Development." Working Paper No. 2014-012, Federal Reserve Bank of St. Louis, 2014; https://research.stlouisfed.org/wp/2014/2014-012.pdf.

© 2017, Federal Reserve Bank of St. Louis. The views expressed are those of the author(s) and do not necessarily reflect official positions of the Federal Reserve Bank of St. Louis or the Federal Reserve System.

Glossary

Factors of production: The natural resources, human resources, and capital resources that are available to make goods and services. Also known as productive resources.

Capital resources: Goods that have been produced and are used to produce other goods and services. They are used over and over again in the production process. Also called capital goods and physical capital.

Standard of living: A measure of the goods and services available to each person in a country; a measure of economic well- being. Also known as per capita real GDP (gross domestic product).

Trade barrier: A government-imposed restriction on the international trade of goods or services.